After years of hype and inflated valuations, and a predictable disillusionment phase, unicorns are making a comeback, but this time, they actually mean something. Beyond funding and partnership announcements, the health and the number of unicorns are other leading indicators of the direction innovation is taking. Indeed, knowing how these private companies valued at over $1B are faring provides us with much more insight than any other subset of companies. On the one hand, looking at new unicorns tells us about the kind of innovations that are scaling up and where investors are betting “big money”. On the other hand, monitoring the health of existing unicorns is a good way to take the pulse of the overall innovation ecosystem.

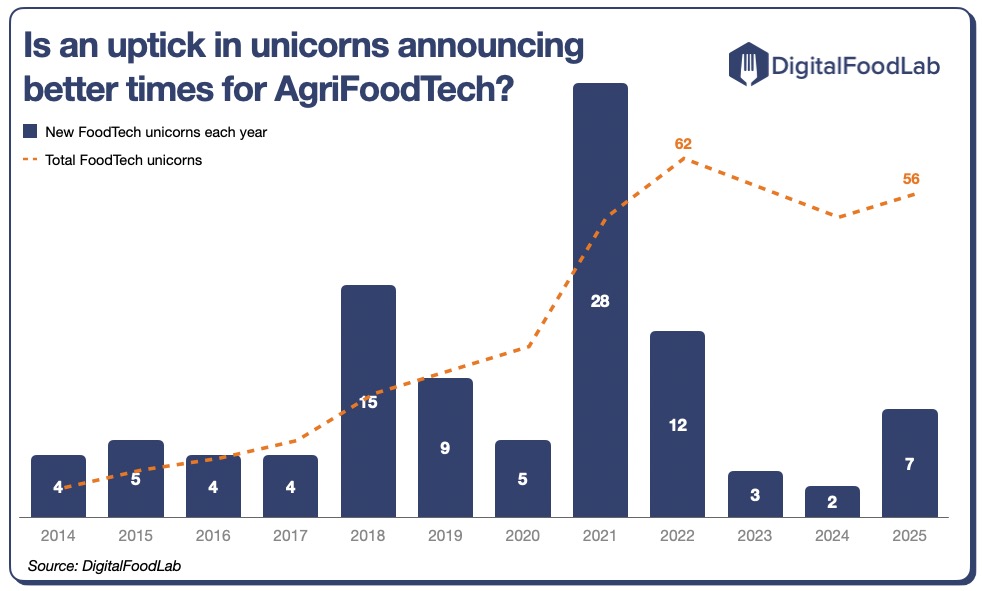

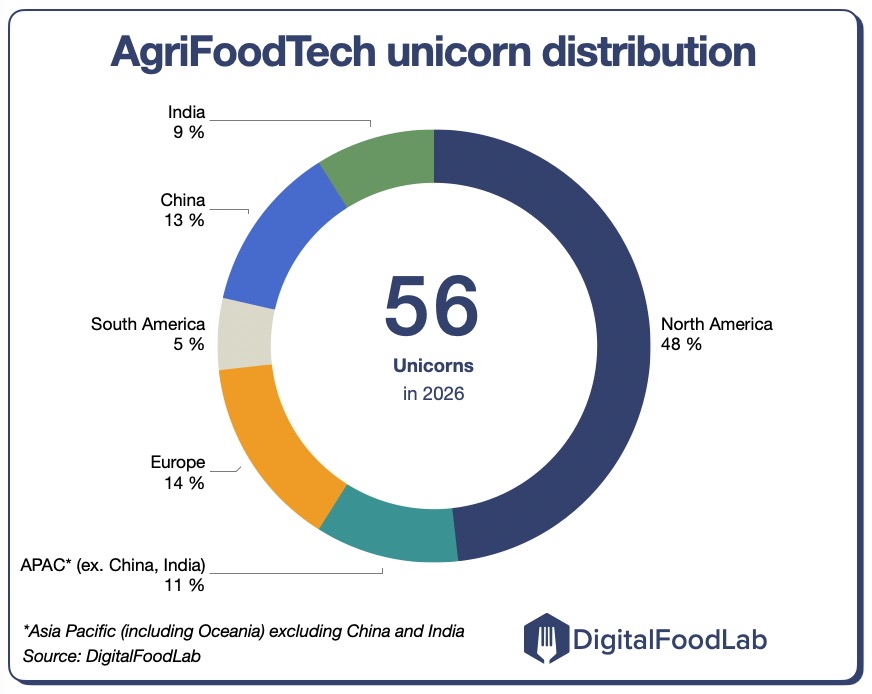

56 AgriFoodTech unicorns in 2026, up from 52 last year

For eight years, we have been following and mapping AgriFoodTech unicorns. The concept has lost much of its mystique and appeal, which, in itself, is a first insight. Until 2022, fast growth and, more importantly, the highest possible valuation were the goals any entrepreneur or investor sought. Four years later, many of these overvalued companies have failed to transform huge funding deals into stable revenue (without mentioning profits). Now, being a unicorn is more than a step in a growth journey; it’s a measure of potential and a validation of business success.

7 new unicorns, a record since the “hype years” of 2021/2022

In 2025, 7 startups crossed the unicorn threshold, a very noticeable feat in a context of stable funding (as shown in our latest funding update). As unicorns often serve as early indicators of the evolution of the overall innovation ecosystem, this increase could also signal a bounce-back for the rest of the ecosystem this year.

7 new unicorns in very different categories

- Nourish, a US personalised nutrition platform connecting patients with registered dietitians through insurance-covered programmes. It focuses on improving health outcomes through scalable, data-driven dietary coaching.

- Halter, based in New Zealand, and which develops smart collars for livestock that enable virtual fencing through sound and mild stimuli. Its technology helps farmers optimise grazing, reduce labour, and improve farm productivity.

- Olipop, a US functional soda brand with prebiotic fibres to support gut health. It positions itself in the “better-for-you” segment with strong retail traction and branding. It crossed the $1B mark after its main competitor, Poppi, was acquired for $2.1B by PepsiCo.

- Fruitist, a US fresh fruit brand (notably blueberries), which has developed solutions to enhance fruit quality, shelf life, and consistency using varietal selection, data, and branding.

- Owner, a US-based platform that enables independent restaurants to manage direct online ordering, CRM, and marketing without relying on third-party delivery apps.

- Ninja is a Saudi-based quick commerce platform offering ultra-fast grocery delivery.

- Jumbotail, an Indian B2B food marketplace that digitises procurement for small retailers and corner stores.

Exits before becoming unicorns

Three startups that came close to become unicorns by reaching a high valuation at the time of their exit (in this mapping, we only focus on privately held startups): Huel (meal replacement) which has been acquired for $1.2B by Danone, Grün (food supplements) acquired for the same price by Unilever, and Once Upon a Farm, a baby and child food brand which reached a $800M valuation at its IPO.

The years of excessive funding and valuations can also be felt inside unicorns. Two companies have been acquired for far less than investors expected: Daily Harvest (frozen meal essentials) and Brewdog (craft beer brand), for only $44M, far less than the $3B valuation it claimed a few years ago. Both are cases of operational errors combined with excessive growth expectations.

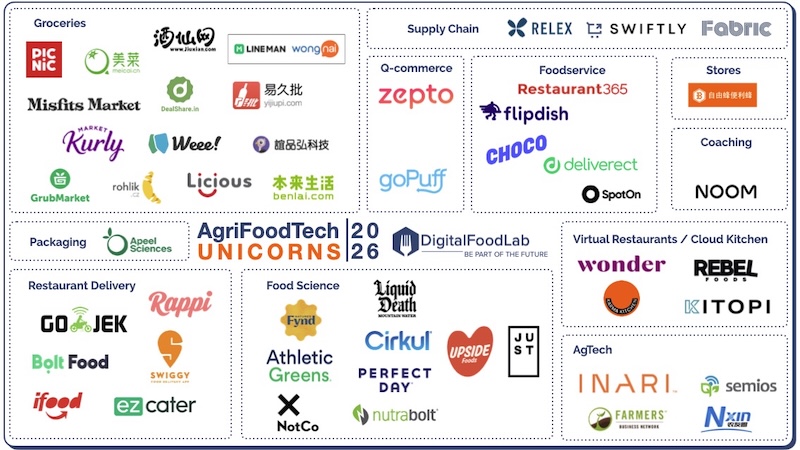

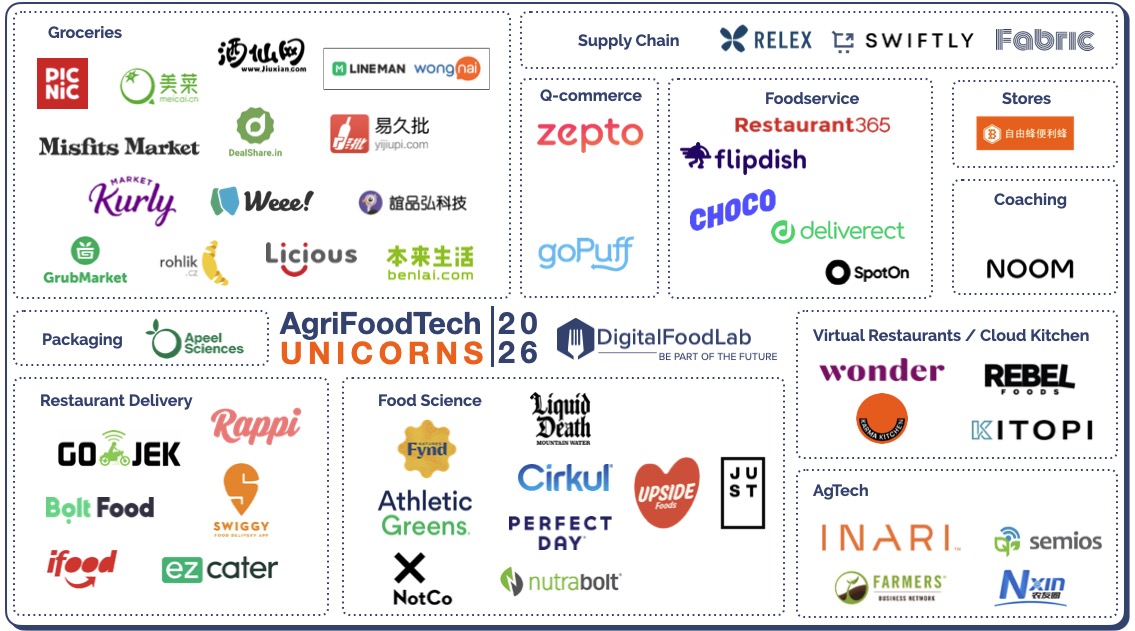

Compared to past years, the evolution is stark. You can have a look at the mapping in 2022 or 2024 to see the evolution. AgriFoodTech is less and less about food delivery and more about agriculture, brands, and food coaching.

Global distribution of unicorns aligned with funding

AgriFoodTech unicorns are distributed exactly as all tech unicorns in terms of geography. Unicorns’ distribution is also pretty much aligned with the distribution of funding, with two caveats that tell us a lot about the structure of different ecosystems:

- Asia, and specifically India and China are doing exceptionally well at creating unicorns, notably in grocery and restaurant delivery. In fact, funding remains quite limited compared to the size of their economies and populations. Instead of being spread across thousands of small-scale startups, funding is highly concentrated on the companies that can benefit the most from the scale of these two continental countries.

- Europe sits at the opposite, with a more limited number of unicorns than it “should have” when looking at funding. European funding is indeed much more spread across companies, with a preference for B2B models and a tendency to favour early exits over growth.

So, why should you care about unicorns?

As explained above, unicorns are a good early indicator of the health of the innovation ecosystem. So, knowing these companies and what they do is an easy way to have a broad idea of where things stand.

It should also be noted that among the startups on the mapping, some could be classified as “zombie unicorns”. These are startups that reached unduly high valuations and that have not raised any funds (or at least not publicly) over the past couple of years, and for whom we have serious doubts about their current valuation. The number is decreasing, as some are getting acquired for sums that look like pocket change compared to their previous valuations, and the others should be “cleaned out” this year.

We observe many positive signs, such as a bounce back and diversification across categories of new unicorns. All of these elements tell a story of resilience and a potential bounce-back for AgriFoodTech.

Finally, the return to grace of unicorns also indicates a potential comeback in high valuations. This should be a sign for agrifood companies that now is a great time to secure partnerships with startups, notably through investments. If valuations increase again, these deals could look very smart in a few months: they could look like a bargain, and even if the partnership doesn’t bear fruit, it could even become financially relevant.