Danone is acquiring Huel, the British meal replacement brand, in a €1B deal. The DTC (direct-to-consumer) is now joining the long list of successful startup food and beverage brands that have succeeded on their journey to stand out as an emerging venture, catching the eye of investors and early adopters alike, then (much harder) generating strong revenue growth, and finally getting the attention of a large CPG company.

Beyond this, the deal underscores the importance of emerging brands as a driver of growth for both CPG companies and the broader AgriFoodTech innovation ecosystem. And more specifically, this is also a story about the journey of a concept and how European companies can win.

1 – What is Huel?

Huel is a meal-replacement startup founded in 2014 in the UK. It offers a range of products marketed as “complete nutrition” that serve as substitutes for whole meals or snacks, from ready-to-drink (RTD) beverages to protein bars

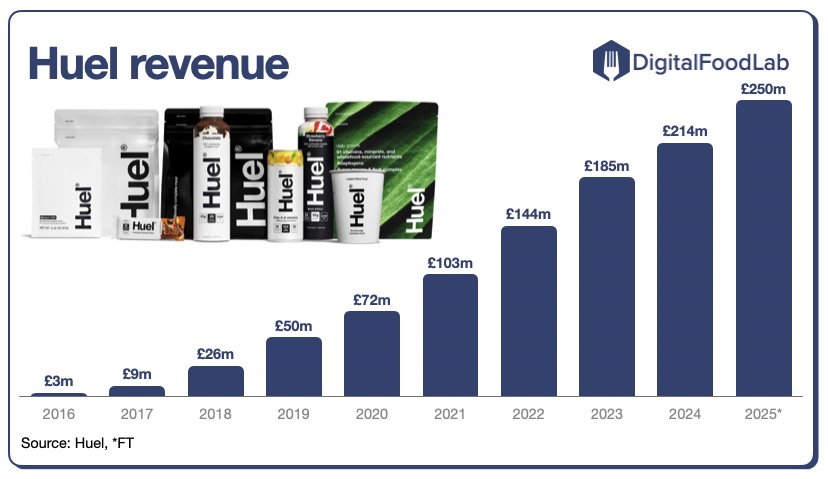

As displayed in the graph, revenue growth has been impressive over the past decade. It raised about £40m between its foundation in 2014 and 2022. In 2023, it raised £82.5M in a private equity deal, rumoured to be a step toward an IPO (a listing on public markets).

Compared to most brands, it has avoided what we call the “four horsemen of the F&B apocalypse” for a young brand, and which individually can kill an emerging brand:

- Profitable online growth: most brands hit a glass ceiling when growing online and never reach profitability.

- Brand expansion without dilution: while initially offering only a single product (RTD), the brand has expanded its product range and customer base. It successfully addressed the needs of busy people and markets, including sport/performance nutrition and weight loss. With its low-calorie solutions and promise of complete nutrition, it has become an ideal solution for GLP-1 drug users.

- Channel growth: Huel is now available at multiple retailers across a selected range (RTD, bars), which is supporting its online sales and growth.

- Internationalisation: it has successfully entered many markets beyond the UK, notably in continental Europe and in the US, where it is now a significant player.

2 – Is it a good deal for Danone, and what does it say about the broader brand/DTC market?

As recently highlighted in our latest insight on DTC brands and M&A, FMCG companies must evolve quickly, and internal growth alone won’t be enough. Looking at the examples of failures and the more limited set of successes, we shared DigitalFoodLab’s DTC acquisition framework. Let’s see how this deal fares against its six points:

1️⃣ Legitimacy: high, but not perfect. Huel has indeed evolved towards supplements recently (with an alternative to AG1) and fits well with Danone’s vision of health through nutrition. This also fits well with Danone’s recent acquisitions, including Kate Farms in medical nutrition, and the potential for Huel to benefit from this to improve its own scientific legitimacy. However, the deal runs counter to the current “anti-processing” trend, as meal replacement solutions are, by definition, highly

2️⃣ Integration: we don’t yet know the details of the plans or the speed of integration, but Danone has shown an ability to slowly integrate players in the past.

3️⃣ International validation: yes, and Huel is at a stage where more capital and the resources of a global FMCG player could help it.

4️⃣ Retail validation: yes, and similarly, it could be boosted.

5️⃣ Right timing: yes, as it was considering an IPO and potential other buyers.

6️⃣ Clear support, growth and exit plan: that we don’t know yet, and that will be the key to the years ahead.

3 – Other companies to follow and a great win for Europe

Huel is following another of our frameworks: the DTC copycat. Actually, it did better than all of the past examples:

- Meal replacement, as a category, was “invented (if we forget about weight-loss products) by US players such as Solyent (founded in 2013).

- Huel “imported” the concept into the UK and launched its first products in 2015. Then, others across Europe, notably Yfood (founded in Germany in 2017 and recently bought by Nestlé), copied the concept again.

What we can learn from this example, and many others like it, including gummies and coffee alternatives, is that there is a pattern where concepts emerge in the US and are heavily funded there. When they succeed, 2 to 4 years later, they are “ready” to expand in the UK and then across the rest of Europe. What is unique about Huel is that the copy has become much bigger than the original.

In a word, this is good news, especially for the European ecosystem, showing that the old continent can be good at creating food brands.

As explained in our predictions for the year, we expect more acquisitions of brands, as food and beverage leaders are reinventing themselves. This is an example of a much larger trend. For companies to follow, you can look at DigitalFoodLab’s list of the most inspiring European AgriFoodTech startups, which includes Huel and a dozen other brands. Also, the chart above shows some of the Global DTC brands we consider the most exciting right now.

In practice, this means that beyond this (short) list, you have to screen these brands as a lever of insights and as potential targets. Spotting, analysing, and sorting them is one thing, but then deciding when to engage (and for what) is another. The question is then: will you spot them early enough, and know what to do with them?