As indicated in our predictions at the start of the year, funding is not coming back to its hype levels, but that’s probably not the most important point anymore. Indeed, beyond the data and the deals, things are moving underground with a renewed appetite for AgriFoodTech topics.

Funding remains stable

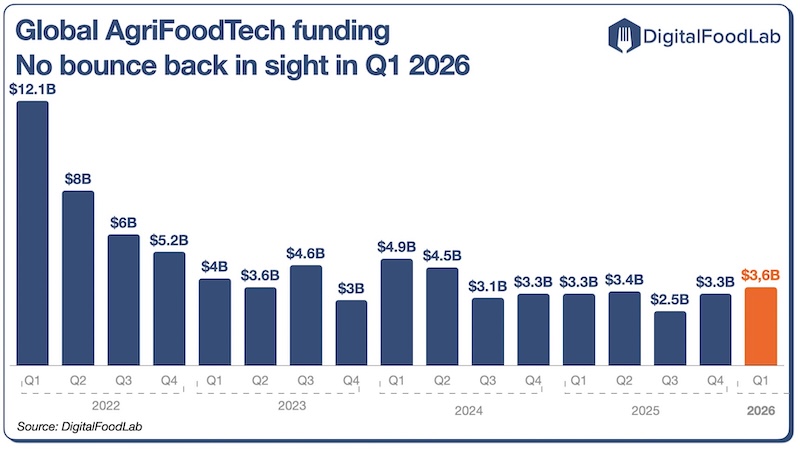

Fact: funding remains stable with about $3.6B raised by AgriFoodTech startups in Q1 2026. As shown in the graph above, funding increased slightly in the first quarter of the year compared to the end of 2025.

Beyond funding, an accumulation of positive signals: as shown below, multiple signs indicate that the situation is improving. The main point is probably the uptick in corporate appetite, which is manifesting in partnerships and acquisitions. The ecosystem remains fragile, but if some of those partnerships start delivering results, we could observe a funding bounce back in the coming quarters.

Geography: a return to an equilibrium between the main innovation hubs

After some movements last year around a couple of mega deals in US startups, we are going back to a more traditional distribution of funding. We observe:

- A bump of funding in Oceania due to the $200M+ deal in Halter (see below)

- An increase in South-East Asia and India around supply chain startups, with a focus on tools to better digitise farmers and help them connect with their clients.

Most interesting deals, acquisitions and partnerships of the quarter

Looking back at all the largest deals of the quarter, here are four key signals:

1️⃣ Corporations are taking back control, with high-value acquisitions (which come alongside the flurry of consolidation deals between large agrifood companies) and partnerships. Key acquisitions include:

- Danone’s $1B acquisition of Huel

- Good Culture, a fast-growing US cottage cheese brand, which received a majority investment from a private equity firm at a $500M valuation

2️⃣ The larger deals were focused on the hidden parts of the value chain, in agriculture and infrastructure:

- Deals to make agriculture less labour-intensive and more resilient, notably Halter, the smart cow collar startup, which raised $220M, and Tropic, which raised $105M for non-browning and disease-resistant bananas, but also many deals around satellite imagery and bioinputs.

- Increased public and private investments in fermentation capabilities, including Unibio’s announced facility in Saudi Arabia, but also funding for precision startups such as Verley, Cauldron or All G.

3️⃣ Emerging brands are reshaping the CPG landscape and answering the consumer demand for innovation:

- In the short-term, as analysed in this insight published earlier this year, and confirmed by the recent stream of acquisitions and investment deals, brands are starting to eat the lunch of major brands, at least in terms of value creation. This is even more visible in brands that are answering new consumers’ needs (performance, GLP-1 companions, processing concerns…).

- For the long-term, with the surge of interest for healthy ageing, and especially, this quarter with a focus on women’s health (through supplements and companies like Biologica, which raised $7M) and longevity, with announcements from leading companies including Unilever’s investment in Novos, and the $100M invested in Loyal.

So, what to expect for the near future?

As mentioned in our predictions, 2026 will be and is already all about scalability. Funding may remain stable in the coming quarters, but this is no longer the only metric to watch. A real shift is happening elsewhere: in the acceleration of acquisitions, in the growing role of corporates, and in the emergence of solutions that are no longer just promises but which are becoming deployable (or at least which will be so in the foreseeable future).

That’s why most investors, as well as large companies, are focused on execution. Every day, we see signs that the desire for innovation for its own sake is waning. Instead, the goal is to find new solutions that can have a concrete impact on tense supply chains, thin margins and wavering differentiation.

In this context, tomorrow’s winners won’t be those who invested or partnered first in startups or in new technologies, but those who are able to demonstrate an ability to leverage innovation now. And, for most companies, this shift is still not really well understood.