Last week, I attended Future FoodTech in London, and the mood wasn’t great, notably among investors. I think it would be fair to summarise my conversations into something like “If you’re an investor in AgriFoodTech and neither an evergreen CVC nor focused on brands, you should at least consider looking at other industries”. By the way, if you want to have my feedback on the event (what I saw, heard, and the impressions I gathered), please contact me and let’s plan a quick chat.

This gloom and doom is, unfortunately, not unjustified. We have just compiled the latest funding data for the third quarter of 2025, and it doesn’t give a pretty picture.

As shown in our recently published report on the state of funding, investments are declining again in 2025. This trend is not reversing in Q3, with a new decline in funding. For the last quarter, only $2.3 billion was invested in FoodTech startups. We maintain our projection for the whole of 2025 at between 10 and 11 billion, which would represent a return to 2015 levels of funding (while considering inflation). While reading this data, please don’t forget that this is not a “FoodTech thing”, but rather an overall retreat from everything that is not artificial intelligence. Recent data shows that a majority of the money invested in startups is now going to AI-focused companies.

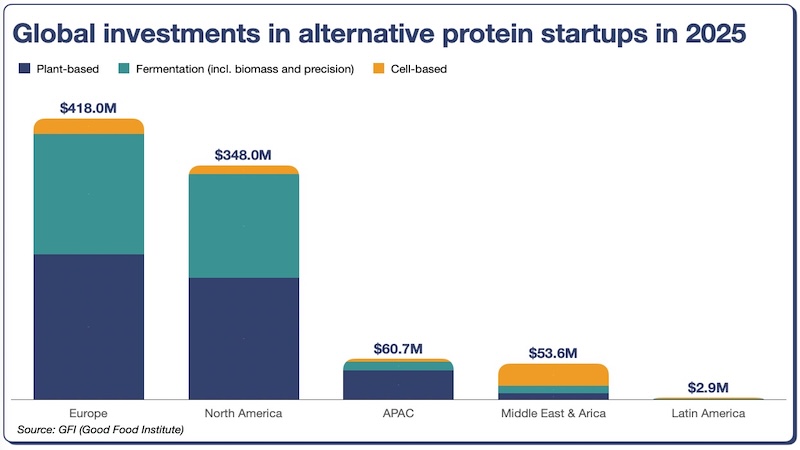

In terms of categories, we didn’t observe significant evolution compared to previous quarters. Delivery startups (notably in Asia and in the Middle East) are raising a bit more due to a couple of large deals, but otherwise things are pretty stable. The only thing that caught our attention was the distribution within the Food Science category, where funding for alternative protein is being replaced by investments in brands, first for beverages, then for protein-enriched food products.

As for the geographic distribution, compared to the first half of this year, two regions stands out:

- Middle East, and more precisely the Gulf region, with a couple of mega-deals: Ninja, a quick commerce startup from Saudi Arabia – $254M in funding – and Calo, a Bahrain-based startup which delivers pre-cooked and personalised meal plans – $39M raised in July

- Europe, with a series of $20 to $50M deals in diverse categories (AgTech with NoFence, Delivery with La Fourche, alternative proteins with The Protein Brewery…).

We don’t expect any noticeable evolution by the end of this year, as all eyes are on AI. However, and that will be my “note of optimism”, things are moving behind the scenes. In the next quarters, here are the three things that I will be following:

- Materialisation of startup and corporate partnerships. As often discussed here, we observed a steep increase in the number of commercialisation and scale-up deals between startups and leading companies across the food supply chain. They have become the new requirement for startups to get the attention of investors. Now, most of these deals are still fresh and have not yet borne fruit, but they can’t disappoint (as most of them did in the past with very little to show after years of discussion). The future of the startups involved (and, to some extent, that of the large corporations too) is tied to them: if they materialise in concrete results (product launches, real commercial orders), this could give a boost to the entire ecosystem.

- Announcements around current hypes. The best sign that AgriFoodTech is still very much alive is the number of new hypes that we observe. The most visible are probably around the three big topics of healthy ageing (sugar alternatives, new healthy ingredients), sustainability (bio inputs, methane reduction, solid-state fermentation), and limited-supply resources (egg, cocoa, and coffee alternatives). All these three topics have matured rapidly recently (notably through partnerships). Concrete announcements concerning their commercial, regulatory and technical viability would be another boost for AgriFoodTech.

- Exits: this is the point where I am the least optimistic, but probably the most important. Ultimately, the health of the innovation ecosystem is closely tied to its capacity to generate liquidity. At this stage, even exits at valuations much lower than expected are welcome, notably in the most tech-driven part of the ecosystem.

If you have any questions about this or would like feedback on the events we recently attended, please don’t hesitate to reach out.