In our latest report on European AgriFoodTech, we showed that the region is not standing still: despite a tougher funding environment, Europe is building strong capabilities in key areas of the food value chain. Alternative proteins and future ingredients are among the clearest examples of this shift. Europe started late, but is now leading. Let’s see why that matters.

We will come back to this broader European dynamic during our webinar on FoodTech in Europe on June 16th (you can register here).

The state of alternative proteins in Europe: a very slow take-off

When we talk about alternative proteins, we are actually covering two sub-categories (here is a more detailed definition of the different technologies involved):

- Proper alternatives: companies leveraging technologies, including plant-based, fermentation, and cellular agriculture, to develop alternatives to animal proteins (and some other ingredients such as cocoa).

- Functional ingredients: companies using the same technologies, but to develop ingredients that have technical (e.g. binding) or health (e.g. immunity) benefits.

While the former remains the most important in terms of funding, we have observed a shift toward most players now promoting their functionalities rather than their ability to substitute for proteins.

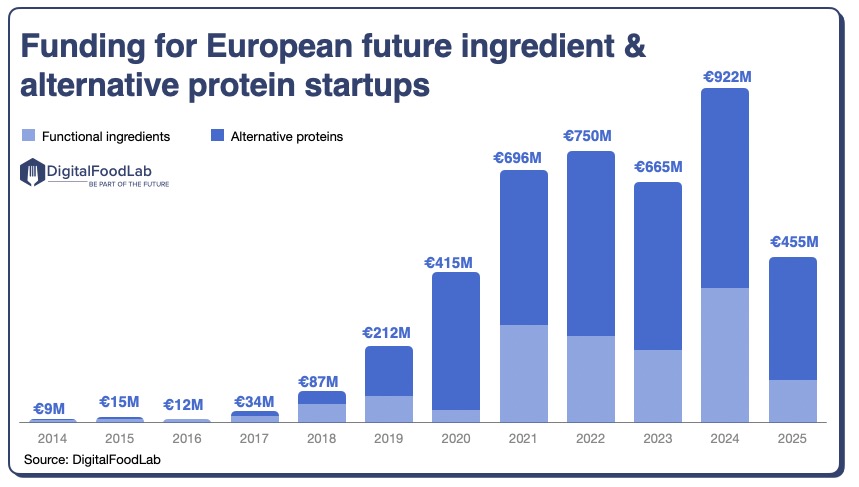

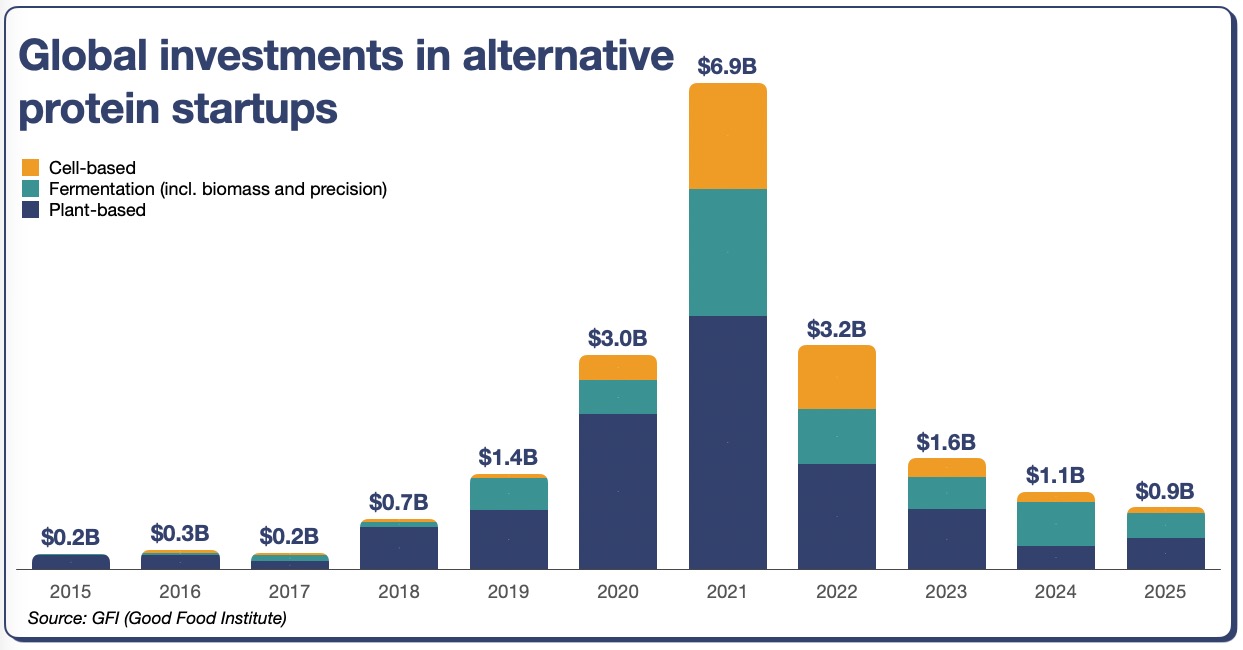

Funding rose from just €9M in 2014, and the take-off was very (very) slow, compared to the rest of the world. When some US and Israeli startups were raising rounds in the hundreds of millions (e.g., $350M raised by Perfect Day, a US startup in 2021), Europe wasn’t really considered relevant to this topic.

But then, as funding plummeted globally by about 85%. When we compare the two graphs, it is striking to see that funding remained quite high in Europe and even with the decline observed last year, it is still at levels comparable to 2020.

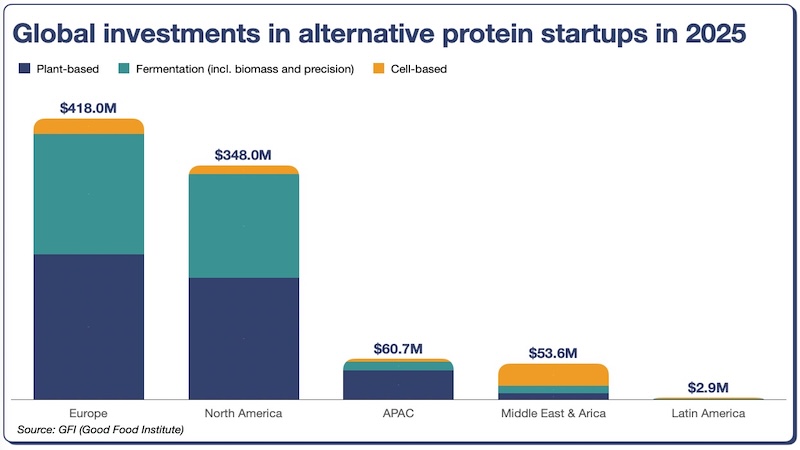

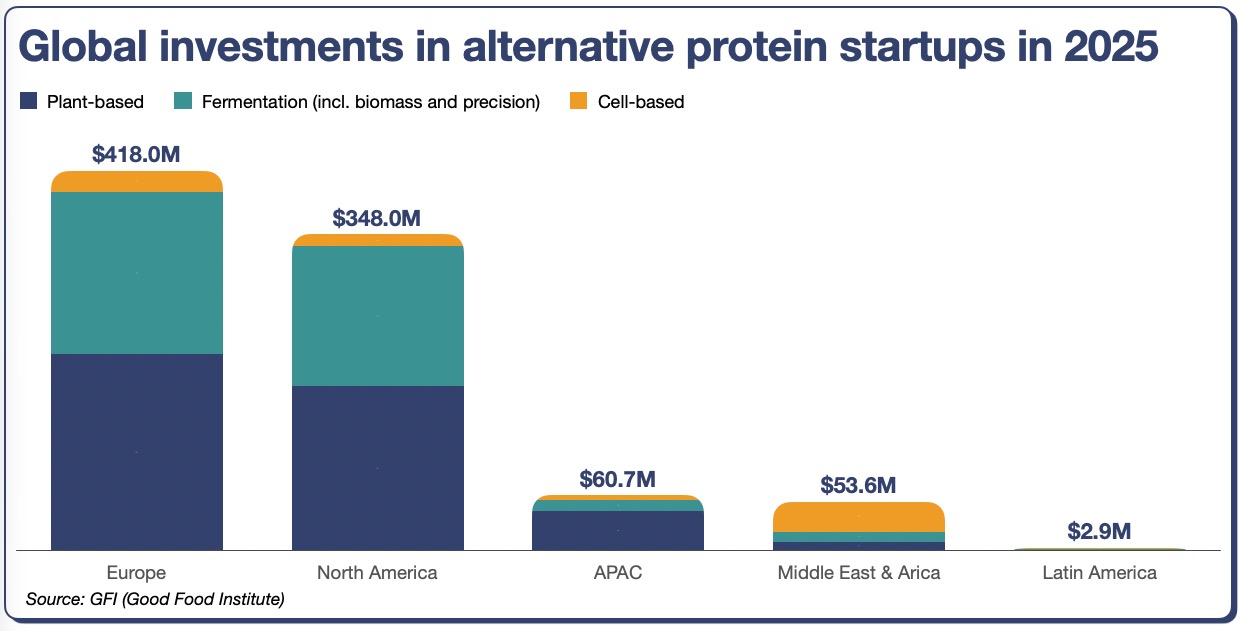

When we look at global investment data for 2025, we see Europe leading by quite some margin, competing only with North America, while the other regions are far behind.

So, what is happening in Europe?

Now, is this just an anomaly, or is there something more to look into? From our discussions and analysis, there are three reasons why Europe is now leading.

1. By starting late, the European ecosystem has avoided the hype

Normally, when talking about innovation, being late is not a good thing… but here it was proved to be very positive. While funding was abundant, it was mostly directed towards startups with huge growth plans, involving early industrialisation of their processes. In most cases, this was fatal to companies that oftentimes had neither a solid technology nor a viable path to profitability. When funding receded in 2022, many players were left with half-finished factories and a market which was not ready for them.

Instead, the European ecosystem, which was never intended for hyper-growth, was much more well-suited to face the funding crunch. This is the case for:

- Plant-based companies which have built fewer capabilities and invested less in marketing (and are benefiting from a market which is growing, while it is decreasing in the US).

- Long-term technologies (such as precision fermentation and cellular agriculture), where startups have always seen themselves as B2B ingredient suppliers rather than potential B2C brands.

2. Public funding supported the ecosystem

When funding receded in 2022, many startups benefited from public grants and loans (such as Formo, a precision fermentation startup in Germany, which received a €35M loan from the European Investment Bank in 2025, or Solar Foods, which received research grants from the EU Commission). This funding was absolutely key, supporting companies and helping convince private investors to bet on European startups.

3. Research organisations oriented towards entrepreneurship

This public funding policy would have been useless if it weren’t for the many European research organisations. Many of them, notably in the Northern part of Europe (such as VTT in Finland), have evolved over the past decade and are now much more forward-looking in their willingness to support entrepreneurship, or even to be at its source.

Europe has indeed built a strange but potentially effective fortress strategy. It combines tough regulation (making it difficult for companies to apply for authorisation in its market) with support for its own innovation ecosystem to become a leading force abroad.

Is Europe’s lead strong enough?

Europe may have been leading in funding over the past couple of years, but the story is far from over. As we have seen, after a first generation of players which mostly failed, alternative proteins are now being reinvented and led by European players. The story could well repeat again. Also, as discussed in our latest insight on China, non-startup players are increasingly important and could dominate the landscape without appearing on the venture funding-round radar.

The biggest limits for European players are regulation and the ability to scale. It seems untenable to have a European leading ecosystem in a continent that doesn’t authorise any of the ingredients for its consumers. One of the consequences (already visible) is that startups and the leading companies buying from them will industrialise production elsewhere, notably in the Gulf countries and North America. This would be particularly disappointing: after funding the research and development of these new technologies, all the commercial and industrial activity would be directed elsewhere.

For now, many global food companies headquartered in Europe are benefiting from this B2B-focused ecosystem (and, let’s be honest, reasonably valued startups) and are announcing an increasing number of partnerships and investments in startups. This should help the ecosystem attract investors and even more international corporate attention in the coming years. In a word, having a map of potential European startup partners is and should remain a key element for agrifood leaders.