We recently held a webinar in the context of Biotech4Food, the European initiative to accelerate the adoption of biotech technologies in the agrifood value chain. It was a great opportunity to think about the growing links between the Biotech and FoodTech ecosystems. While it’s easy to confine Biotech to the realm of pharma and MedTech, the technologies developed there, such as microbial fermentation and molecular farming, have now become key to the food industry. While this convergence is becoming increasingly apparent for startups and investors, it creates multiple uncertainties for incumbent businesses.

1 – What do we mean when we talk about the intersection of FoodTech and Biotech?

If we go back to the basics, biotech can be split into three spaces:

- Red biotech: medical and healthcare applications

- Green biotech: agriculture (bioinputs, livestock health, new crops)

- White biotech: industrial processes and ingredients.

Another way to look at the intersection is to consider the different FoodTech spaces where biotechnologies are being used.

As shown in the above DigitalFoodLab’s trend curve, FoodTech and Biotech intersect in almost all the most forward-looking trends, notably in these three megatrends:

- Resilient Farming: making farming more sustainable and resilient to climate shocks requires the development of bioinputs and biostimulants (often leveraging micro-organisms to substitute chemicals), feed additives and vaccines to reduce methane emissions from livestock, and genomic engineering for crops.

- Sustainable ingredients: to develop alternatives to animal proteins and ingredients to alleviate shortages (coffee, cocoa…), biotechnologies such as precision fermentation (mostly named microbial fermentation in the pharma space) and molecular farming (or pharming) are used. Interestingly, when moving from the pharma space to food, the names have been changed, as if to try to make these technologies look more cutting edge than what they actually are.

- Healthy ageing: this last megatrend, which notably seeks to develop a new range of food ingredients that can have a positive health impact (new sugars, GLP-1 companions…) is the most visible testimony of the growing convergence of the Biotech and FoodTech spaces.

2 – A long-lasting trend that won’t fade away

Not all FoodTech trends are born equal, as some wither away before being given the chance to be really experimented with. However, in our case, everything is pointing towards a greater “Biotechification” of FoodTech and indeed of agriculture and food in general.

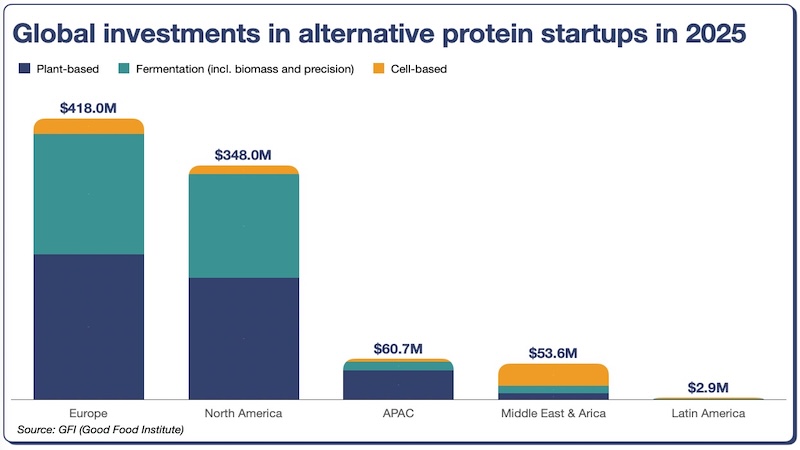

Helped by growing support from public organisations and governments, biotechnologies are often seen as one of the key technologies of the future, a source of wealth, highly qualified employment through re-industrialisation, and competitiveness. This explains why most developed countries have recently announced plans to support the scaling up of the biotech industry, most of them explicitly including agriculture and food applications as a key component of their strategy. Just in the past 12 months, the EU announced a €350M, followed by some EU national plans, the UK, South Korea, China… while the US already has a multi-billion-dollar strategy established.

3 – Serious strategic implications for agrifood leaders

For most large agrifood companies whose value relies on marketing and process capabilities, this is a total change of paradigm. Waiting until startups and other innovators develop the technologies enough for them to be ready to pick up, as any other ingredient won’t cut it.

There are multiple paths that agrifood players can follow, among which the three most obvious:

- Partnerships + supplier relationship: CPG companies can avoid entering this space and follow the usual pattern of leveraging new ingredients developed through biotechnologies in their products. However, this is a high-risk scenario: if the new ingredients (notably those with health and sustainability benefits) become recognised by the consumer, the value will follow, and these companies would see their margins shrink.

- Interested buyer relationship: by building capital relationships with biotechnology players, industry leaders can spread their bets and better prepare for potential shifts in their value chain.

- Integration: by directly owning (by internal development or more usually by acquisitions), industry leaders can better integrate the value created by biotechnologies. While the rewards are high, the bets are much more costly. This is, however, what many upstream players (agriculture inputs and ingredient suppliers) are currently doing.

Navigating this increasing complexity requires a clear vision of the different trends and an honest assessment of a company’s capabilities. It also opens many opportunities and markets (such as the ones we recently explored in this insight). But, in a word, if today an agrifood company has not yet developed its “biotech strategy”, that is something they should do very soon.