As we are nearing the end of the year, now is a great time to reflect on what happened over the past 12 months, to review what we learned during the year, how the predictions we made at the start of the year fared, and think about the perspectives for 2026 for the agrifood industry.

I think the word that best summarises this year is “crossroads”, as the agrifood industry and the AgriFoodtech innovation ecosystem are both facing many of them. Looking at the year in the rearview gives us some ideas of where we stand, and more importantly, of what lies ahead.

1 – The agrifood industry is at a crossroads, and it is not looking good…

As shown in the graph below, based on a recent survey, US consumers are simply trading down across most food-related categories. It’s not that they are eating much less, but rather that they are buying cheaper stuff, notably in the categories where agrifood businesses make the highest margins: snacks, soda, alcohol…

We are here because of a combination of factors, notably:

- Agrifood businesses have been much more quickly impacted by the current rising tariffs than other industries (where it was possible to stockpile many things). And, in many instances, consumers are wary of possible price rises, saving more, and cutting on the most immediate thing they can: their food budget.

- Inflation’s aftereffects are still there, with consumers still feeling negatively about the recently rising prices.

- Climate shocks and shortages of many products (eggs, cacao, coffee, beef…).

- GLP-1 drugs’ rising adoption (consumers simply eating fewer calories and redistributing their purchasing power).

- Backlash against sustainability efforts, notably in the US.

These elements have weighed negatively on F&B and commodity companies for quite some time now. What’s new is that it is also impacting the margins of ingredient companies. And, in the short-term at least, all these factors are here to stay. This is a crossroads moment for the whole industry, which in many ways needs to reinvent itself.

In a word, 2025 has been a transition year. The year was still dominated by a focus on cost reduction and on maintaining market share (through increased marketing efforts). Beyond, the industry is now much more focused on:

- a push towards healthier products, both to answer consumer demand (as illustrated by the chart above) and to create long-term differentiation.

- finding alternatives to face shortages.

2 – The innovation ecosystem has also evolved to answer those needs

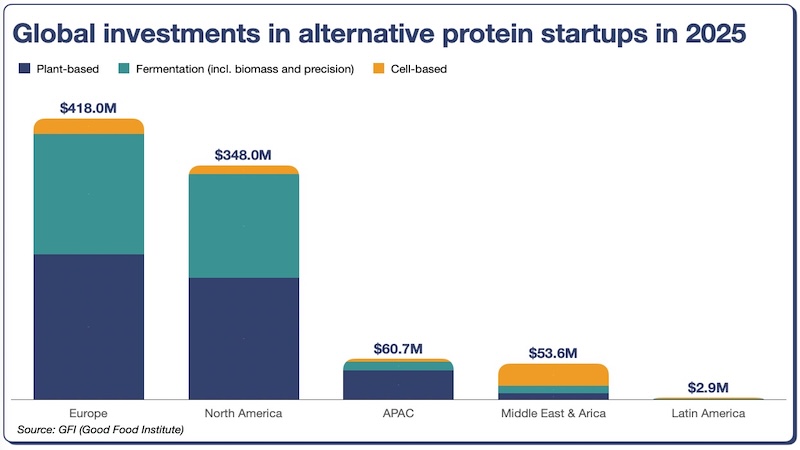

While we mostly discuss the state of the AgriFoodTech innovation ecosystem, it is increasingly important to contextualise it by examining the industry itself. Indeed, if funding has declined by almost 80% since peaking in 2021, this is in significant part due to the absence of exits.

And that can only change if the innovation ecosystem answers the needs expressed by consumers and businesses. This year, even if the investment landscape remained gloomy, it looks like the two sides have finally connected meaningfully. Startups are more focused on addressing industry challenges. We have observed a surge in commercialisation partnerships that should, hopefully, yield results in 2026.

3 – 80% score on our predictions for the year

Another way to look at the year is to assess the set of forecasts we made in January (you can find them here). Reviewing this list of 7 predictions shows we did quite well and reinforces the idea that food is at a tipping point. We predicted that:

✔️ The context would remain negative and lead to bankruptcies for alternative proteins, notably plant-based, and for vertical farming.

✔️ AgTech as a whole would do great (notably agriculture robots), alongside Food Science applications in materials, cosmetics, and healthy ageing: these have been, with the exception of materials, the categories that performed the best during the year, with now (too) many startups plastering cosmetics on their decks.

❌ High uncertainty on regulation for alternative proteins and an increasing number of controversies: actually, the noise created by the new US administration shook things in the right direction, with many countries moving towards more open regulatory frameworks to position themselves as biotech hubs.

✔️ Large agrifood businesses to keep moving more partnerships with mature startups, matching identified needs, and providing much less support for younger ventures. The number of partnerships announced has been impressive… as has been the decline in engagement with the more early-stage part of the ecosystem.

½ New extreme climate events will create new hypes: cacao and coffee have been joined by a few new ingredients on the “target list for alternatives”, notably eggs.

✔️ Health, regenerative agriculture and AI would remain the main themes of the year, with more focus on implementing that “talking”. 2025 was the year of acquisitions and portfolio moves focused on healthy snacking and beverages. Similarly, many companies doubled down on their regenerative agriculture commitments, even amid a sustainability backlash.

So, what should we make out of this? First, this was a very intense year, full of movement and uncertainty… and it will probably stay that way in 2026. Questions about health, sustainability, and demographics will continue to challenge the current growth model of the agrifood industry. For industry leaders and innovators, it has become a necessity to deliver a vision of where they stand at this crossroads and help others understand the future.