We just released our European FoodTech report. European AgriFoodTech startups raised €3 billion in 2025. But, increasingly, the story is not in the numbers but in what’s behind them. Today, we’ll cover our three main takeaways from the report and the perspectives for the year ahead.

1 – Funding keeps declining, but the fundamentals remain solid

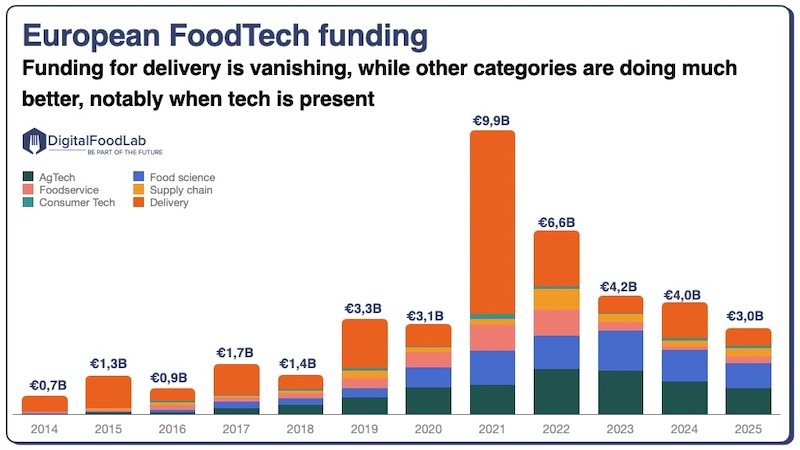

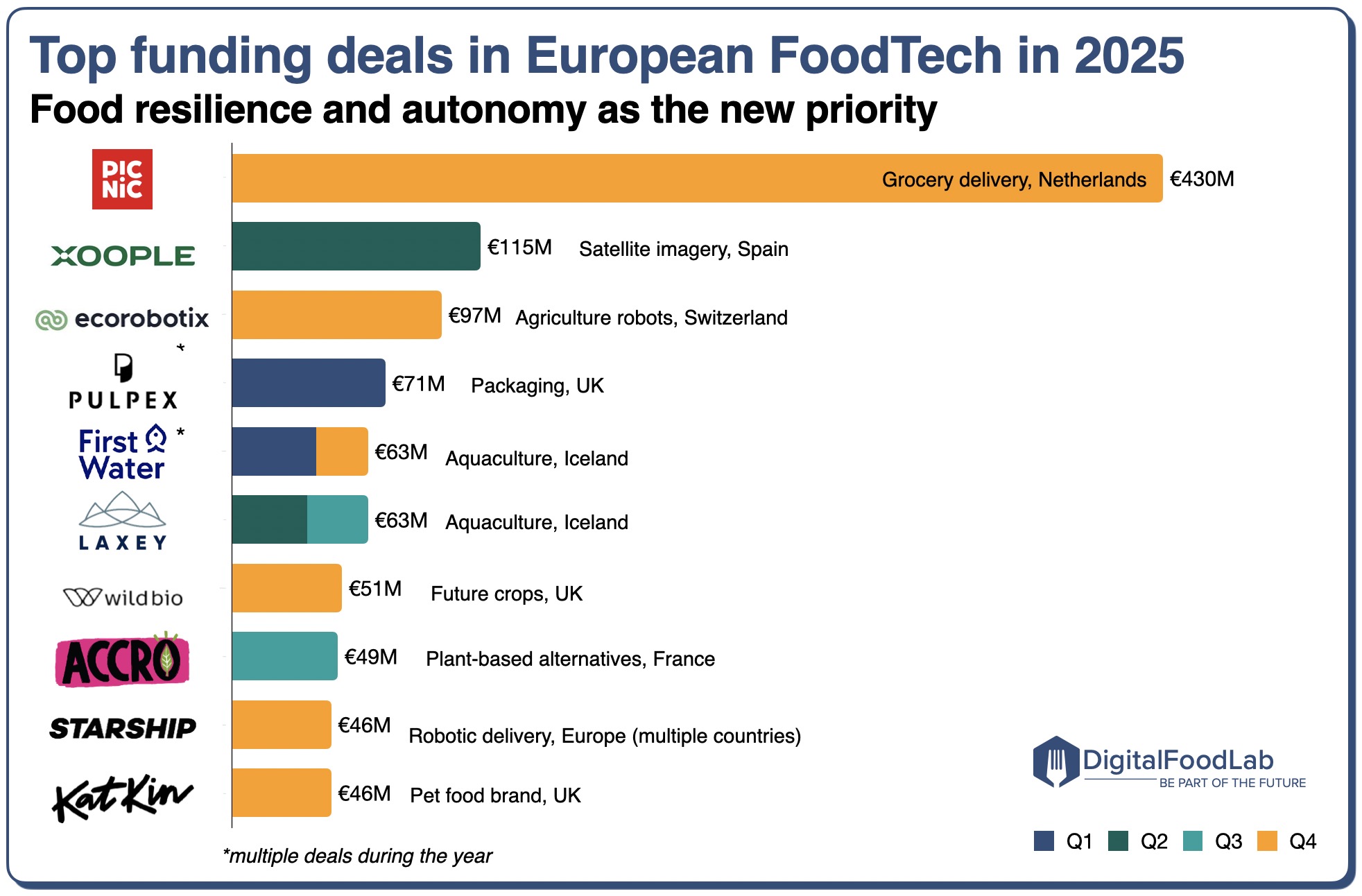

Funding for AgriFoodtech startups dropped (again) by 25% between 2024 and 2025, confirming a return to the pre-hype levels.

Beyond raw investment data, there are many positive signs:

- A global hub for innovation: Europe continues to perform well relative to the rest of the world and now accounts for 28% of global AgriFoodTech funding.

- Long-term conviction in the ecosystem: early-stage funding (investments in emerging startups raising their first rounds) remained stable. This means that entrepreneurs (with investors betting on them) are still creating new waves of emerging projects with long-term potential.

2 – New key categories and new hubs

One of the defining features of European FoodTech is the absence of a single, well-established hub of innovation. Instead, there are many competing locations, each with its own logic, governmental incentives, and corporate support. While this is not the best approach to create global leaders, this competition has its own merits and is pretty efficient in times when funding is scarce.

This is well illustrated by the “podium” of national ecosystems. This is notably the case with the rise of Spain, one of the most interesting agrifood innovation hubs, with exciting startups across the whole value chain, from agriculture to ingredients, to new brands. At the other end, usual leaders, and especially Germany, underperformed.

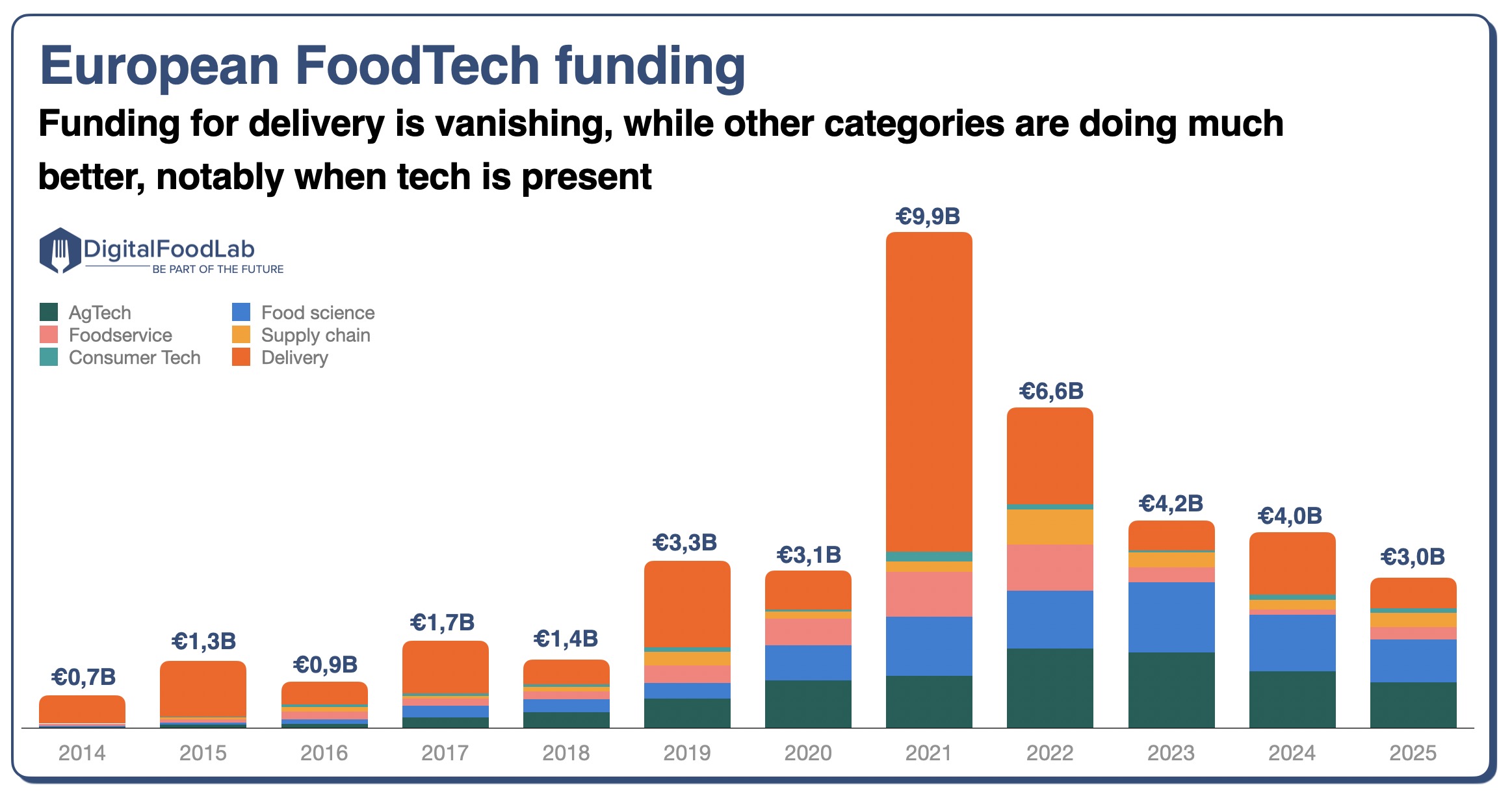

As shown in the funding graph above and in the list of the top deals for the past year, this is also a story of investments in AgTech and Food Science rather than Delivery. This is driven by multiple factors, including:

- Aqualculture: infrastructure deals in Iceland, Norway and Finland to build large-scale aquaculture farms are supporting AgTech funding.

- Food resilience, which is emerging as a strong theme across the continent, and which is indirectly helped by rising defence funding (many startups such as Xoople, formerly centred around the use of satellite imagery for agriculture, are refocusing on defence).

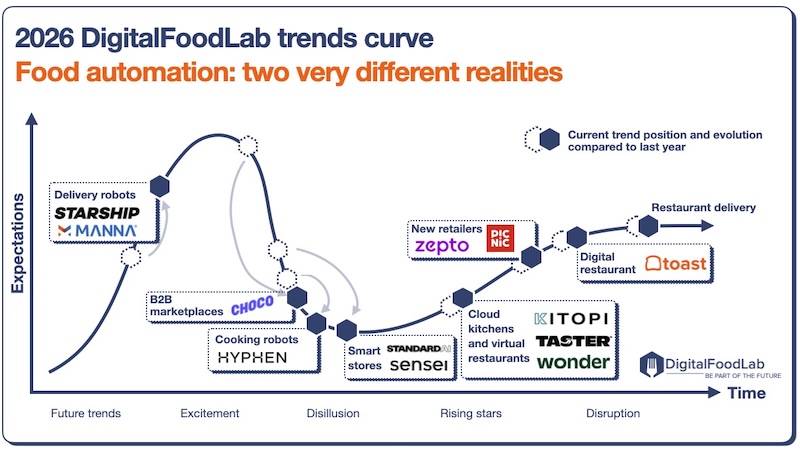

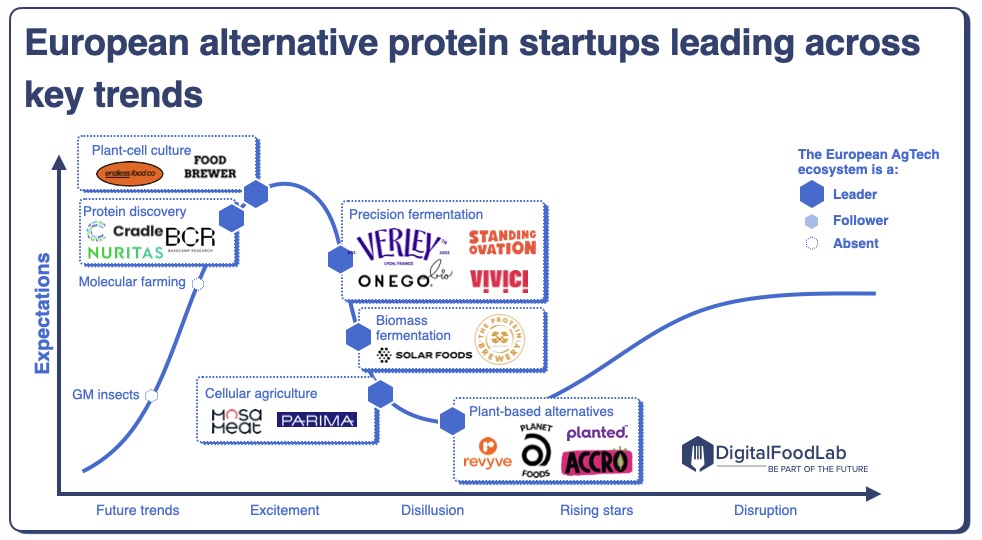

- Alternative protein and new ingredients: while global funding for new proteins fell sharply, Europe is building strong positions in key technologies and becoming the dominant hub, notably for fermentation technologies (as shown with the examples on the trends curve below). European startups, with the B2B-first model, have proven to be well-suited to the current funding environment.

- DTC Brands: from plant-based (whose sales are still rising in many European countries) to pet food and beverages, we observe the first hints of “European DTC brand moment”, which could become much stronger in the next couple of years.

A structural challenge remains unsolved: Europeans startups are increasingly strong in many advanced technologies… but then they commercialise in the US

Things are far from being perfect for European FoodTech startups. While we measure an increasing number of European startups signing deals and partnerships with global companies, in most cases, this is about commercialisation outside the continent.

In key areas, ranging from biological agricultural inputs to precision fermentation to delivery robots, European startups are often ahead, but as in most of the examples mentioned on the trends curve above, when required, they are seeking (and gaining) US regulatory approvals and see their path forward in the US and Asia.

Beyond commercialisation, this also translates into industrialisation efforts. A good example is the fact that multiple alternative protein startups have recently announced plans to build large-scale facilities in the Middle East.

From a corporate perspective, this is quite positive, as it shows the agility of European startups and their capacity to find the market where it is and to be open to partnerships with companies from across the globe. From a European perspective, it raises questions about the continent’s ability to truly benefit from the innovations it has generated.

What’s the situation after a decade?

Time is flying: this is already the 9th edition of this report. With a decade in the rearview, the evolution of the European FoodTech ecosystem is quite impressive. Once heavily focused on delivery and foodservice software startups, it is now diverse and leading in many of the most advanced technologies. This has been aided by European-level grants and the development of institutions (such as VTT, VIB, and others) that support the “translation” of research into startups.

However, most structural challenges remain; notably, the absence of a unified capital market, combined with strong cultural and regulatory barriers, complicates the emergence of large-scale companies.

From a corporate perspective, this is again not such a negative situation: European startups need corporate support to scale, and even more to commercialise their innovations abroad. That’s why we expect involvement from agrifood companies worldwide, with European AgriFoodTech startups continuing to grow.

Download the 2026 European FoodTech report with a full breakdown by category, stage, country, and trend curves with lists of the most relevant startups to know.