I am glad to share our yearly global FoodTech investment report with you. While most of its contents are not especially optimistic, it is important to have a clear view of the state of the innovation ecosystem to be able to address its many challenges.

You can download the full report here.

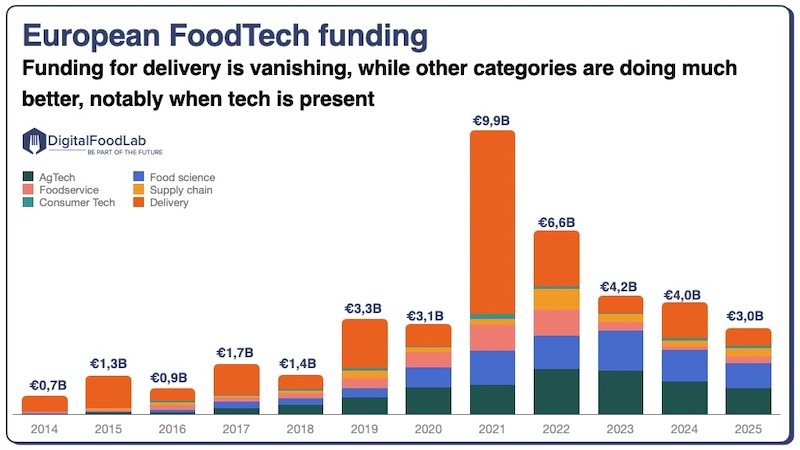

After a small rebound last year, investments are again declining

Let’s look at the big picture of global AgriFoodTech investments. We can clearly see that while investments dropped after the 2021/22 excitement, they rose again in 2024, supported by some very large deals and a stronger-than-expected end of the year. However, since the start of 2025 and the rise of economic uncertainties, investments have severely decreased again.

AgriFoodTech investments have just gone back a decade in terms of volume and returned to 20215 levels. A new source of concern is the sharp decline in pre-seed and seed funding (investments in emerging startups): while investments rose overall in 2024, they declined by more than 31% for early-stage deals. While the average deal size is declining, what we observe is a steep decline in the number of deals.

This translates to an ever-growing “lack of faith” in the future potential of AgriFoodTech from the part of investors and entrepreneurs alike (there is less funding in part because at the beginning, there are fewer startups to finance.

More positively, the current decline in funding is partially compensated by a stronger involvement of public players (notably through large investment plans in biotech) and large agrifood companies through partnerships. Also, brands are doing spectacularly well. Over the past year, we observed more than $10B in acquisition volume, with more than $6B being for innovative brands. In all cases, these had a wellness or healthy ageing element attached to them, showing the great appetite of larger companies for this topic.

As shown by the graph above, last year’s increase in funding was primarily due to delivery deals, and more precisely to a handful of megadeals. As for the first half of 2025, the decrease is felt across all categories. Some ecosystems, such as alternative proteins, have seen investments almost come to a halt in the past few quarters.

Finally, in terms of geographical distribution, the contraction is not evenly distributed. The share of investments going to US-based startups is reaching its highest point ever at 59% for the first half of 2025. US FoodTech investments even rose in the first half of 2025 and could surpass last year’s. At the same time, Europe’s share is retreating to 12%, erasing all the progress made since 2021.

Looking at the current situation, we don’t expect the situation to improve significantly before mid-2026. At that stage, and after four years of funding decline, only the startups with the strongest value proposition will remain. If, in parallel, the early-stage ecosystem is preserved, we would then be in a healthy state to prepare the future of food.

Our recommendation for everyone interested in the success of this innovation ecosystem (and its positive consequences on our health and environment) would be to push for these three elements:

- More early-stage venture creation and funding (notably through tech transfer)

- More private-public funding of large-scale infrastructure

- Positive incentives/regulations to encourage the adoption of innovation.

These can be applied by governments, companies, universities… and would be a game-changer. In the meantime, you can download the full report here.