Last week, in our predictions for 2026, we forecasted funding would be flat. As long as current economic headwinds and investors’ preference for AI-related topics don’t evolve, we’ll remain in the current intermediary state the AgriFoodTech ecosystem has been in for the past three years. We have just compiled the data for the last quarter of 2025. As for the rest of the year, it appears normal, but there are interesting moves behind the main data points.

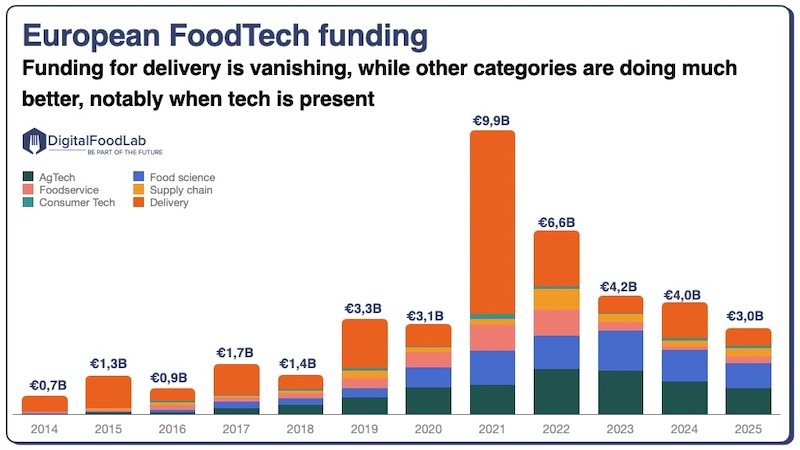

After a bounce back in 2024, AgriFoodTech funding is declining again

Fact: decline in funding, again. As shown in the graph above, funding declined again in 2025 to a level almost equal to that of 2023. The small bounce back observed in 2024 was indeed due to a handful of megadeals at the start of the year.

Analysis: more positive news than we could have expected a year ago. In the current context, I think this graph should be interpreted with some optimism, and more with a “half-full glass” view. Let’s remember that there are currently many reasons for investors NOT to bet on FoodTech, including recent failures (in insect proteins, vertical farming, alternative proteins, and quick-commerce, just to name a few), a low-reward environment for risky investments, and a preference for AI. Also, the increase in the number of partnerships between large corporations and startups, both for commercialisation and scale-up efforts, reduces the latter’s need for funds. In a word, observing stable AgriFoodTech funding for the third year in a row almost feels like positive news.

US startups are doing well, others much less so

Looking at the 2025 investment distribution, it was mostly driven by US startups, which had another strong year. In this context of stagnation, this was mostly at the expense of European startups. In terms of categories, some trends are still attracting a lot of attention, with both a rising number of deals and increasing investment amounts. That’s especially the case in some pockets of the alternative protein and AgTech ecosystems.

Delivery deals are still leading

Grocery delivery, notably quick commerce (Zepto, Ninja, GoPuff), remains the category attracting the largest funding rounds. It is, however, quite interesting and telling of the trends shaping the innovation ecosystem to have a non-alcoholic beverage (Arkay, a whiskey alternative) and a startup developing genetically engineered crops (Inari) among the largest deals.

Many exits and bankruptcies

2025 was also an impressive year for exits, with a range of healthy brands acquired (Poppy, Lesser Evil…) and of bankruptcies.

With about 80% less funding than in 2021, many companies that were unable to become profitable or raise additional cash are reaching the end of their journey. This was notably the case of multiple vertical farming startups (Plenty, Infarm, Aerofarms), alternative protein startups (Meati, Stockeld Dreamery, Believer Meat), and insect protein companies (Ynsect, Agronutris). Combined, these 8 startups alone had raised more than $3B.

So, what’s next?

AgriFoodTech is holding up better than expected in 2025. Behind the headline numbers, the innovation ecosystem has transitioned and has reached a new equilibrium: fewer bets, fewer illusions, and hopefully fewer excesses. Increasingly, startups are reaching deals with larger corporations because they demonstrate real traction and relevant technologies.

Looking ahead to 2026, we expect more of the same, with clear winners and losers in most categories. We’ll see more partnerships, more products reaching the market, more proofs of viability, industrial pilots, and ultimately acquisitions.

For corporates, this phase creates both risks and opportunities. First, there are fewer startups to work with, increasing the need to identify and secure the right partnerships early. On the other hand, the market is becoming much clearer, making it easier to distinguish companies with real chances of scaling from those that won’t.