This week, we selected four graphs that capture the different time horizons shaping the food system.

On one side, consumer priorities and commodity markets can shift rapidly. On the other hand, agricultural practices and food innovation are evolving much more slowly. Understanding these different timelines (and aligning expectations) is essential to set realistic expectations about how the food system can change.

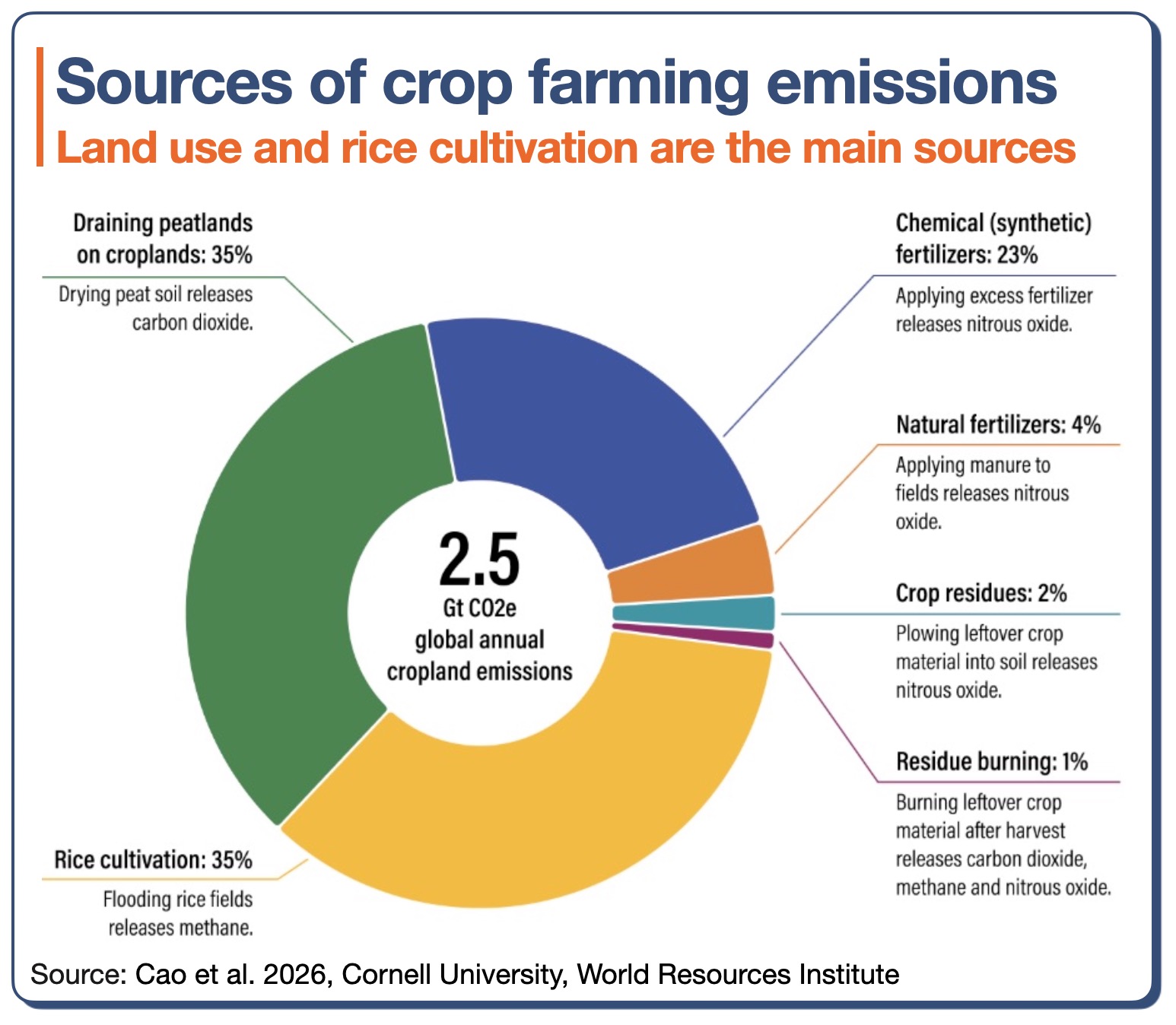

1 – Long-term and hard to shift: the environmental price of crop farming

While we often mention the impact of animal farming on the environment, which accounts for about 15% of total emissions, growing crops also takes its toll. A recently published dataset and maps from Cornell University show that emissions from cropland are far from negligible. First, they account for 5% of global human-caused greenhouse gas emissions (much more than aviation). Then, they are highly concentrated with:

- 67% of the emissions coming from four crops (rice, maize, wheat, and palm oil), but the distribution is quite surprising.

- 61% of the emissions coming from six countries (China, Indonesia, India, United States, Thailand and Brazil).

And, as shown on the graph, three agricultural practices dominate emissions from crop production:

- Peatland drainage: when peatlands are cleared and drained for agricultural production, such as in Indonesia for palm oil cultivation.

- Flooded rice cultivation, which releases large amounts of methane.

- Synthetic fertilisers use.

Crop production increased by 50% between 2000 and 2020, while cropland emissions rose by “only” 17%. Productivity gains are not enough to reverse emissions growth. As the population continues to increase this century, more energy should be invested in supporting and financing the transition away from more emissions-intensive practices.

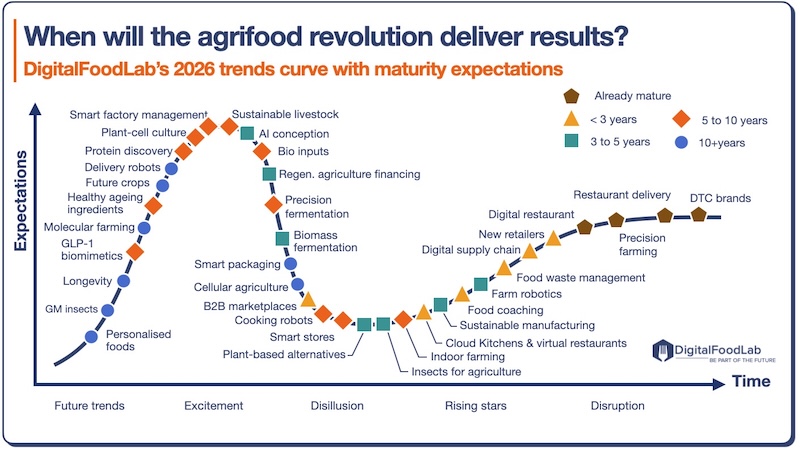

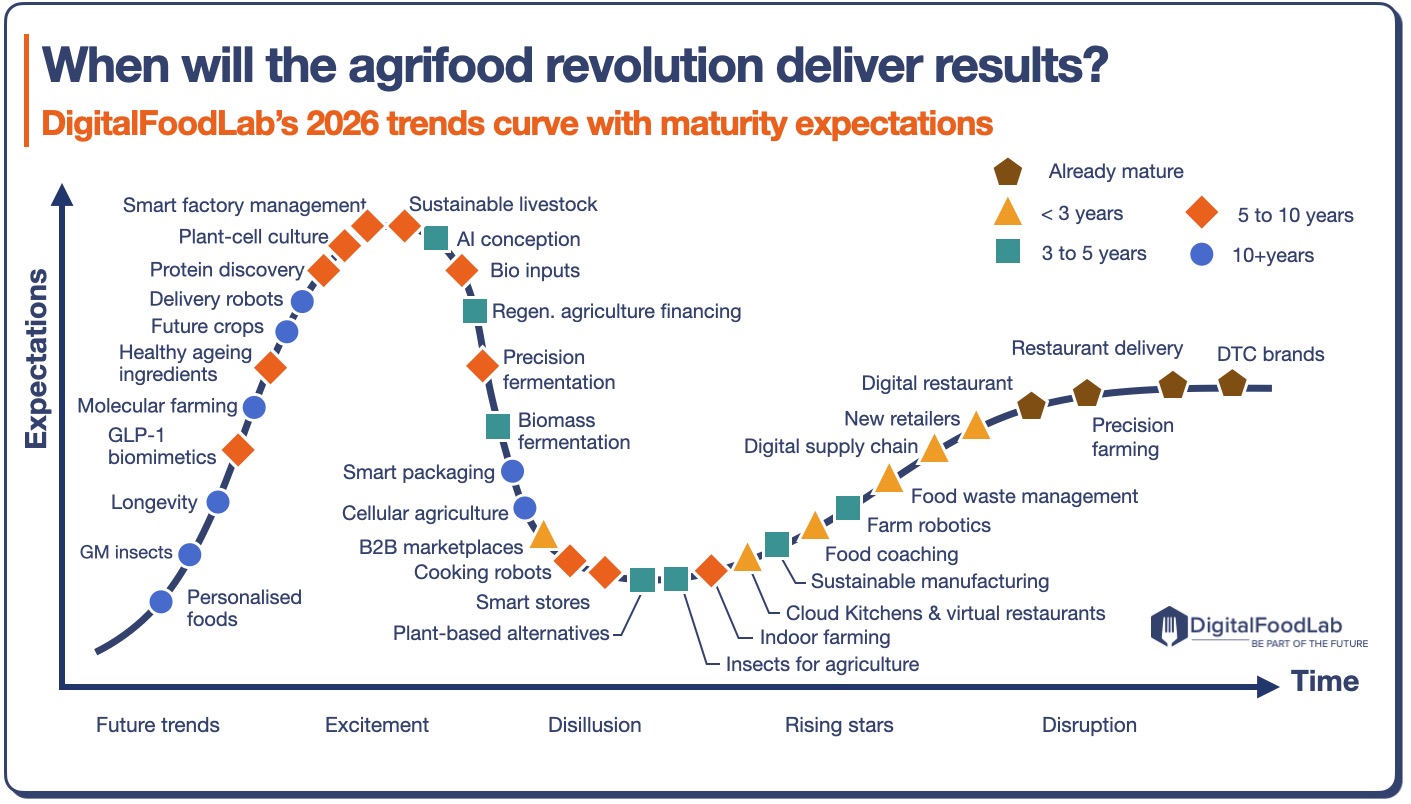

2 – The long timeline of innovation: when is the future coming?

Last month, we published DigitalFoodLab’s yearly report on the trends shaping the future of food and agriculture. One way to look at these trends is also to consider when they will have an impact.

The graph displays our estimation of when each of the 36 trends will enter maturity, or put in another way, when its applications will be:

- Viable from a technical and economical point of view

- Widely understood and understood by its beneficiaries (a good rule of thumb is to have 30% of an industry using a new technology).

There is almost an alignment between the position on the curve and the timeline, with the bulk of the most disruptive technologies having an impact in an horizon in 5 years or more. For instance, even if alternative protein technologies are moving forward, they will still take some time to have a real impact. We should never forget that “food is a long game” and that the industry is very complex to disrupt.

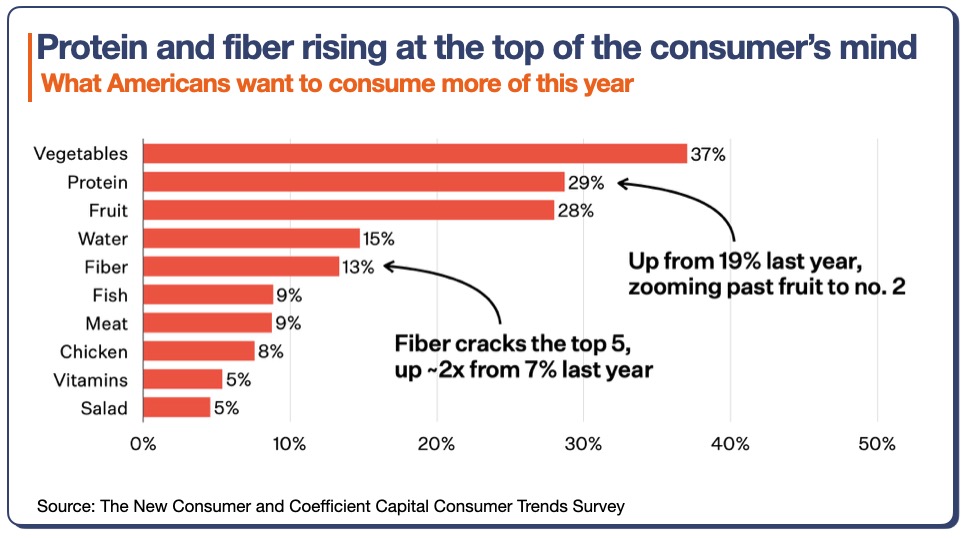

3 – Short-term consumer signals: protein and fiber are rising at the top of the consumer’s mind

A recent survey of American consumers asked them to name the three products they would like to consume more of this year. While many of them are still looking to eat fruits and vegetables, it’s the other answers which are worthy of our attention :

- 29% of respondents want to eat more protein, 10 points more than in 2025 at the same period. The number of people mentioning fish, meat or chicken is noticeable (I am surprised that so few people are looking to eat more ice cream or cheese, I’d love to see the results of the same question asked in different countries).

- 13% mentioned fiber, which is becoming “the new protein”, with a growing number of products displaying how much they contain on their packaging.

- 15% thought about water, boosted by the “hydration” trend and the belief that we don’t drink enough of it.

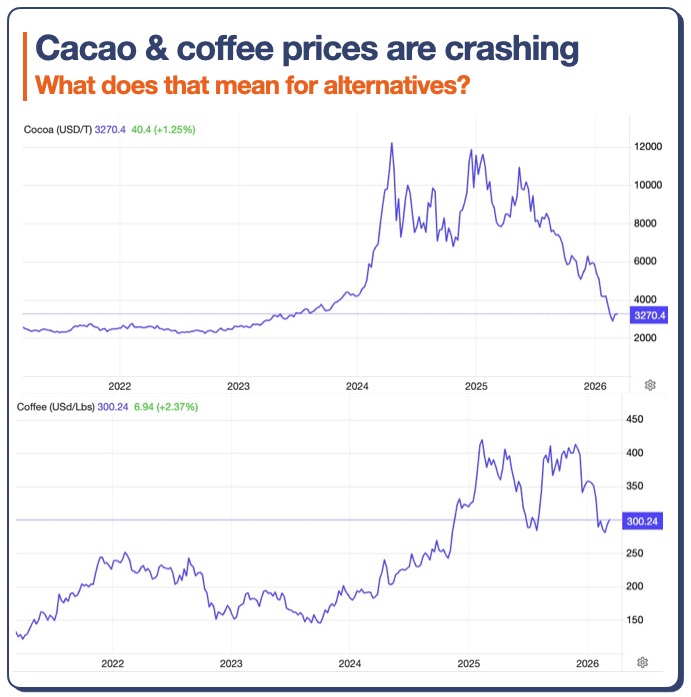

4 – The fast pace of commodity prices: cacao prices are crashing

Cacao and coffee prices have skyrocketed in 2024 and 2025 (x5 for cacao, x3 for coffee) due to a combination of factors, including climate shocks and unmet demand. As both supply chains return to normal, prices are slowly returning to pre-crisis levels.

As explained in our detailed insight into coffee alternatives, a whole ecosystem has emerged with a range of short-term to long-term solutions to substitute both products. As the price bubble bursts, we do not expect a similar deflation in the appetite for alternatives. Actually, there are structural challenges that make alternatives relevant:

- Climate events such as those observed over the past years are almost sure to come back, and to have a similar impact as supply chains are tight with a rising demand for both commodities.

- Climate impact: both products have a high environmental cost, notably due to land use.

- Geopolitical risks (such as the recent tariffs on coffee).

In a word, for commodity players and food companies, having a set of alternatives to include in their portfolios and eventually leverage if prices increase again is great insurance against volatility.