With the end of the year approaching, if some are at risk of an overdose of chocolate, my personal risk is spending too much time at conferences talking about the state of the FoodTech ecosystem and making projections for the years ahead. There is, though, a benefit of all these talks, I see which messages resonate with the current mood, and as often, the actual situation is quite different from what is felt. What’s different now is that, compared to previous years, the innovation ecosystem is probably doing better than what is perceived.

1 – On paper, things are looking quite bad…

I like to start my talks by providing a view of the state of the ecosystem, both in terms of funding and trends. And, indeed, if we look at funding alone, things are doing poorly on most fronts:

- less money getting invested

- (much) fewer startups being founded and funded

- growing concentration in a single area (North America) to the detriment of others, with some regional hubs almost vanishing from the landscape, thereby reducing innovation diversity.

There is no way to sweeten it: with 5 times less money available than 4 years ago, many startups have to shut down. The reduced pool of capital, combined with the absence of exits in many categories (except for innovative brands and agricultural robots), is making the situation extremely complicated for most players.

That’s maybe me being French and insisting on things that don’t work (if it works, there is no use in talking about it, no?), but oftentimes, I see that this is the only message that gets through to an audience. However, there are many reasons to stay optimistic.

2 – But it’s not that bad

There is a French saying that goes along the line “Looking at ourselves makes us anxious, but comparing ourselves to others reassures us”. And indeed, if we broaden the scope, FoodTech is not doing that badly compared to other ecosystems.

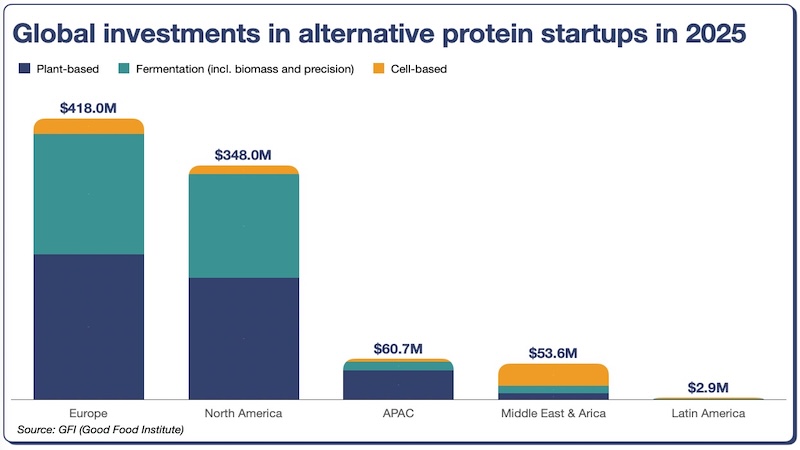

As you can see on the graph above, FoodTech is doing exactly “as bad” as Tech, excluding artificial intelligence (AI).

Nowadays, investors are flocking to everything related to AI. And even though most startups are adding AI to their decks, the link between AgriFood and AI remains thin. Don’t get me wrong, I know that many applications and disruptions will come from AI, notably those that we have listed in this previous insight, but in most cases, AI remains more of an enabler than a core technology.

Anyway, even if there are some specificities to FoodTech, things are not worse than in other ecosystems. Being “not worse” is a meagre reassurance, but it always helps to put things in context.

Comparisons can also be extended through time. If we look at previous funding cycles, the current slowdown is far from being the worst. In the aftermath of the dotcom bubble or the great financial crisis of 2008, startup funding declined to the point that entire ecosystems were wiped out.

3 – Beyond the gloom and doom, things are doing quite well

The final, but probably most important point, is that recently, things have been getting better for AgriFoodTech:

- Even more emerging trends and technologies disrupting food and agriculture: as we are working on our revised trends/hype curve for 2026 (here is this year’s edition of our report – let us know if you’d like to be among the first to discover the update), we are observing a multiplication of the number of emerging trends.

- Increasing number of corporate partnerships through investment and commercialisation deals: this is my main driver of optimism, as corporate involvement is now essential for products to reach the market and make a real impact. Many of these partnerships are pointing toward 2026 as a pivotal year where many products will finally be used commercially, which could create a new positive cycle.

- Regulatory updates: since the start of the year, tens of startups have received regulatory approval in the US, Australia, China, and even very recently in Europe (if Europe, the ultimate laggard in terms of alternative protein approvals, is moving forward, that is a sign that things are changing, don’t you think?).

Beyond these factual points and the doom-and-gloom of the funding situation, there is a sense that the worst is behind us. AgriFoodTech is “cleaned” of many of its excesses and is now ready to enter a new phase, combining disruptive innovation from early-stage startups with the emergence of commercially and technically viable solutions prepared to scale. Beyond the timely “end-of-the-year optimism”, this renewed faith in the potential