FoodTech in Europe - 2026

Investments, innovation and trends report on the state of the European FoodTech in 2026

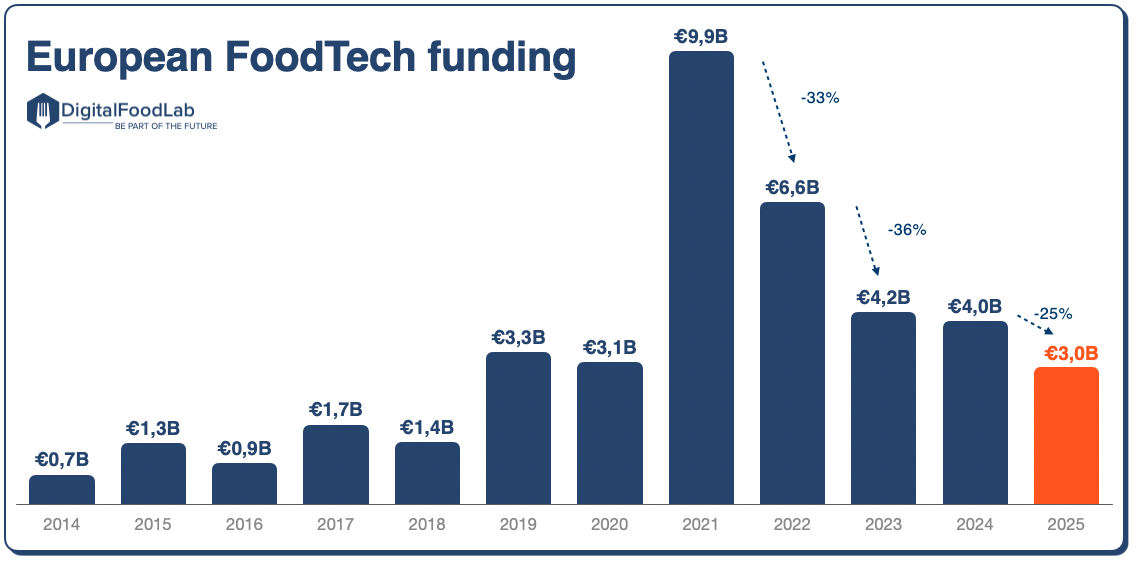

Funding is back to pre-excitement levels

European FoodTech startups raised €3B in 2025, a 25% drop from 2024, confirming a return to pre-hype levels. This stabilisation should not be misread. While funding dropped by 25% in 2025 and deal count declined by 20%, the fundamentals remain solid: Europe now captures 28% of global FoodTech investments, confirming its position as a leading innovation hub.

Three structural shifts define this year:

Upstream wins. AgTech and aquaculture absorbed a disproportionate share of capital, driven by infrastructure deals in Iceland, Norway and Finland. Funding for resilience (food security, bio-inputs, farm robotics) is becoming the new anchor of the ecosystem.

Alternative proteins are gaining strategic importance. While global funding for new proteins fell sharply, Europe is building strong positions in key technologies. European startups, with their B2B focus and regulatory pragmatism, are better positioned than competitors in the US or Asia for the current market.

Geography reshuffled. The Netherlands led thanks to Picnic's €430M mega-deal; Spain solidified its place as a rising hub; the UK and Germany underperformed. Robotic delivery (Starship, Manna) and precision fermentation are European strengths, but their commercial scale-up is happening in the US.

The key question for 2026 is not funding recovery, it is ecosystem renewal. Even if early-stage funding (Seed, Series A) remained stable, signalling long-term conviction in the ecosystem, with fewer early-stage startups being created and fewer deals across all stages, Europe must rebuild its pipeline to remain a global leader beyond this cycle.