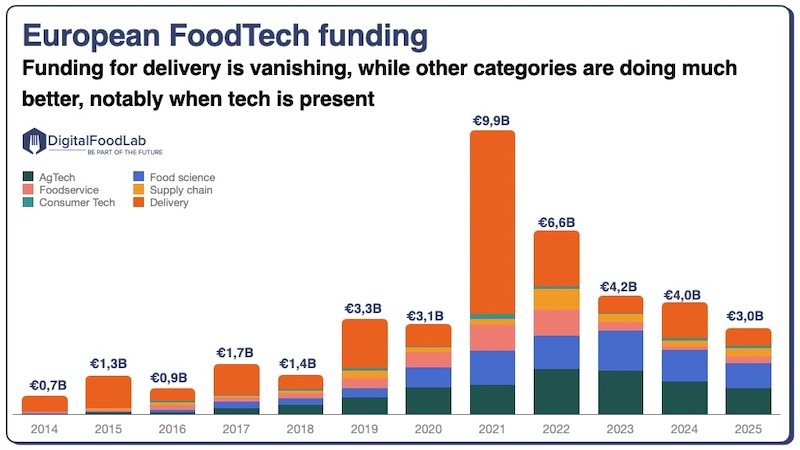

We recently published a detailed update on the state of the investments in FoodTech startups (globally and in Europe). In the second quarter, they declined again globally to reach $2.7B, less than a third of what we measured a year before. I am optimistic that investments will bounce back in the next few quarters.

However, beyond this data that reflects the overall health of an ecosystem of thousands of startups, the consequences of this decrease are also getting much more tangible. In the past weeks, many startups that raised huge amounts of money at staggering valuations during “the good times” in 2021 are facing a much harsher reality. We can draw (at least) three lessons from these recent examples.

1 – Consumers don’t value convenience and sustainability as much as many expected

It would be too long to list all the quick-commerce (rapid grocery delivery from hubs inside city centres) that failed in the past two to three years.

Most assumed that at some point, concentration would occur and then that by rising prices slowly, they would reach profitability. Concentration did happen, but unfortunately, restaurant delivery companies (Deliveroo, Uber Eats, DoorDash) were already entering the market, creating a new wave of competition. At the same time, consumers were not ready to pay a premium for the difference between 15 and 60-minute deliveries.

Let’s look at two examples:

- Frichti, a French meal delivery and quick-commerce player initially bought by Gorillas, was acquired last week for a value of $30k (and $450k for its stock). This startup had raised $56M. Its acquirer will now deliver in one hour instead of 20 minutes.

- Jokr, a US-based startup, was agile enough to close its operations in its home country and open new hubs in Latin America. There, convenience has a greater value (and labour costs are much less problematic). The startup has recently raised money at a $800M valuation. That’s less than previously, but still, it is a lot of money.

In a very different market, Indigo Ag, which specialises in sustainable practices for agriculture, was recently valued at $200M, down from $3.5B. For all its innovation, the market seems to move slower than anticipated. As for the broader ecosystem of carbon credit startups, while relevant on principle, if it does not make economic sense to the farmer and the eventual buyer (often food companies), it will not work. And to work, it requires that the consumer pays more for a more sustainable product. Some are ready to do it, but as we can see today, that’s more a niche than the bulk of the market.

I often think there is a lot of wishful thinking on the part of some investors and entrepreneurs: convenience and sustainability. Convenience is a “nice to have” but not something that most consumers are ready to pay more for.

2 – Getting bigger will not make you profitable when you operate a business with limited economies of scale or if your market is not ready. Tech & logistics will.

Again, let’s look at two diverging examples of meal kits (delivering weekly boxes with all the ingredients to cook meals)

- Blue Apron, one of the meal kits historic leaders, will be acquired by Wonder (a unicorn with its own challenges) for $103 million. The company went public in 2017 for $1.9B. That’s quite a hard pill to swallow for its investors.

- HelloFresh, initially a German copycat, is doing surprisingly well. It even reported a double-digit profit rise for the second quarter of 2023. It is now valued at around $5B. Compared to Blue Apron, it had a much stronger supply chain, offering more choices and flexibility to consumers,

As for quick-commerce, it shows that it’s not impossible to succeed in low-margin businesses for food startups: it’s just a logistics nightmare, and very few players will succeed.

The same thing could be said for vertical farming, even if success seems even more evanescent here. Infarm, Europe’s most well-funded vertical farming startup, has been declared bankrupt. It is, however, rumoured to have raised $40 to $50M from a Qatari fund. Previously, Infarm had raised $604M. What’s fascinating about vertical farming is how many startups received funding to build their farms without proof of viability at a lower scale. I often think that investors get confused with food: a farm is not like software; there are, of course, economies of scale, but just not as much.

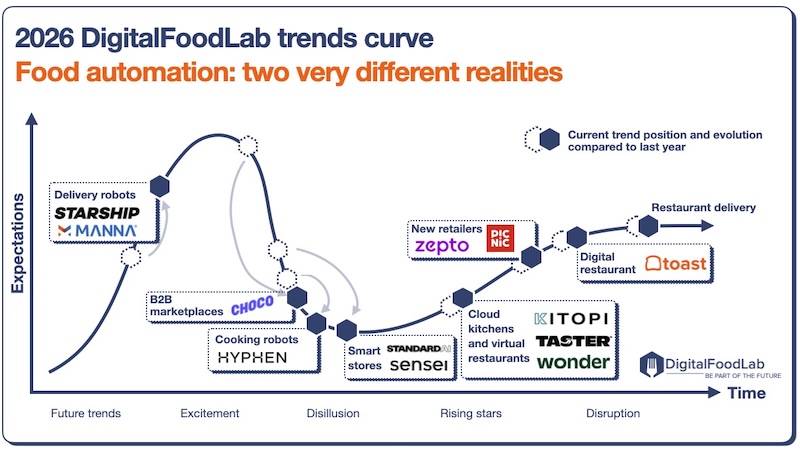

3 – Being agile, having a focus on either a niche or tech can help to survive most situations

As I said above, I am optimistic for the overall FoodTech ecosystem. Investments will bounce back. And even for the categories mentioned, hope prevails:

- There are two horizons for vertical farming: in the short term, companies positioned as technology providers for indoor farms are doing quite well. In the long term, climate change and its impact on crop yields will create opportunities for developing technologies that are neither profitable nor working today. For example, recently, Asahi’s CEO was warking about upcoming beer shortages due to declining barley crop yields in Europe. This or producing high-quality ingredients could be the future of vertical farming.

- Quick-commerce is probably not a viable model for delivery for developed economies, but it remains relevant in developing countries. And “new retailers” are still taking market shares to established players, primarily by focusing on tech and logistics to be more competitive.

In a word, in the future, don’t always believe that because a company has a multi-billion valuation, its investors and founders have a solid plan to become profitable. Sometimes, it’s just pure luck, sheeplike behaviour and buzzwords.

And last but not least, it’s normal for startups to fail: that’s even “part of the game”. It’s the opposite that wouldn’t be normal. For each startup that successfully impacts its market, hundreds have failed. The goal is not efficiency but rather speed and maximised impact. Employees and founders of failed startups will have gained experience and knowledge that may become the basis of future successes.