COP26 ended this weekend on a bitter note and some tears due to a weaker than planned agreement. While this is somehow unsurprising, it is nonetheless a disappointment. As was the fact that farming was not on the agenda. For example, if a deal has been struck on methane reduction, the goals mainly mention the emissions linked to fossil fuel extraction and transport, not those due to animal farming (which alone represents 18% of the global greenhouse gas emissions).

And beyond global warming, the pandemic has shown all over the globe how stretched and fragile the food supply chains were. That’s why in our recent report on FoodTech Trends we identified The resilient farm as one of our top megatrends. Multiple trends are driving us toward a more sustainable and resilient farm: the growing appetite for proximity, climate change concerns notably in terms of arable land, and the convergence of technology and farming.

This trend is going in two very different directions:

- First, we observe a trend toward making the current farm smarter and more efficient, notably with precision fermentation and new crops (with higher yields and protein content) and new animal feed. It is also becoming more resilient with robots to perform repetitive and arduous tasks (for example, weeding performed by startups such as Naïo).

- Second is the space comprising urban, indoor, next-generation farms. These startups are bridging the gap between the point of production and the consumer and reducing the space needed to grow food. And again, they offer cities a chance to become more resilient by growing food inside their limits.

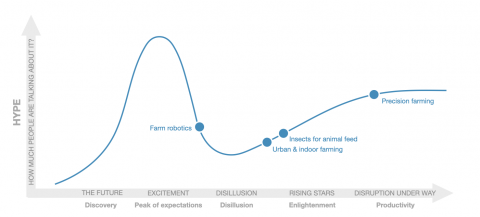

It is always interesting to see the difference between the “hype” and what entrepreneurs do (and what investors finance). If sustainability is key (and regenerative agriculture discussed), it seems that resilience (and hence autonomy) is a much more suitable word to discuss the future of agriculture.

Finally, a precision: it has always been DigitalFoodLab’s conviction that AgTech is a part of the FoodTech ecosystem and not a standalone ecosystem. Indeed, we see more and more convergence and integration in the farm-to-fork value chain. For example, without a more resilient farm, there is no future for most of the alternative protein technologies without innovation in new crops (to feed cultivated meat startups’ cells or precision fermentation companies’ bacteria).