Recently, I am getting more and more questions about the meaning of FoodTech. Beyond the definition we wrote with DigitalFoodLab in 2016 and the various six categories (and 30+ sub-categories! all defined here), these questions address exciting points. That’s why I would like to answer two of the most common today:

1 – What is FoodTech, and what are the “limits” of the ecosystem?

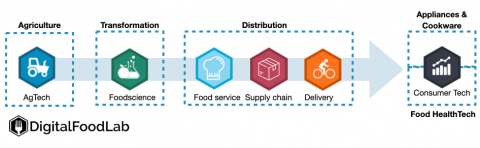

For us, FoodTech is the made up of all entrepreneurs and startups innovating all along the food value chain, which means that:

- AgTech (startups making the current farm more efficient or inventing the farm of the future) is then a part of FoodTech. That is key for us as the speed of innovation increases. It creates a need for downstream and upstream players to understand each other better. An example is the emergence of a robust ecosystem of startups working on innovative crops (notably with higher protein yields or without an aftertaste) to enable the development of better-tasting plant-based products.

- FoodTech is bordered by many grey areas, such as biotech startups working on peptides that can be used on crops or for health, financial services for restaurants, or personalization services that verge on MedTech. Beyond making poor debates (believe me, you don’t want to argue over that), this matters if you want to compare consistently ecosystems between them year after year.

- Short-term and longer-term projects cohabit in this ecosystem. On one side, you may have companies developing new food brands, and on the other one, startups working on deep tech. Their path to profitability (and exit) diverges widely.

- Being a FoodTech startup does not necessarily require having a “tech” behind it.

2 – What makes a FoodTech startup a startup?

Indeed, what have in common a startup working on crop solutions, one selling CBD drinks, and a company developing a connected coffee machine? Beyond the fact that they bring innovation all along the food value chain, for us, a FoodTech startup is either:

- in its infancy, a company whose business model is not to earn money but to gather knowledge on its consumers, product, or technology. It spends others’ money until it hopefully has a product that people are ready to buy (the famous product-market fit)

- then, it is a fast-growing company. By fast, we mean something around 5 to 10% per month for seed startups and 2 to 3% in later stages.

In a word, FoodTech is still a pretty young and somewhat messy ecosystem. And I really think that is part of its beauty and interest. It is hard to navigate all the intricated and often contradictory trends (such as the emergence of a strong ecosystem of companies developing insect-based animal feed versus the growth of alternative protein startups). That’s why looking beyond the current hypes is necessary to develop a clear understanding and a strategy.

Do you have any questions on the FoodTech ecosystem, its limits, and, more importantly, why and how you should prioritize it in your strategy as an ag, food, or retail company? Contact us!