Over the past year, funding for alternative proteins decreased sharply, but good news has appeared on another front: regulation. Many companies have engaged with regulators, and some received approval. So, what’s the state of regulation today?

First, a word on “alternative proteins”. These are still the words used to qualify this ecosystem born around… proteins. But today, it is more than that, with most of the funding going to startups developing substitutes for ingredients such as sugar, fat, oil, flavours, coffee, etc. That’s why we now prefer to talk about sustainable ingredients. The technologies are those developed for alternative proteins but applied to a much larger range of ingredients.

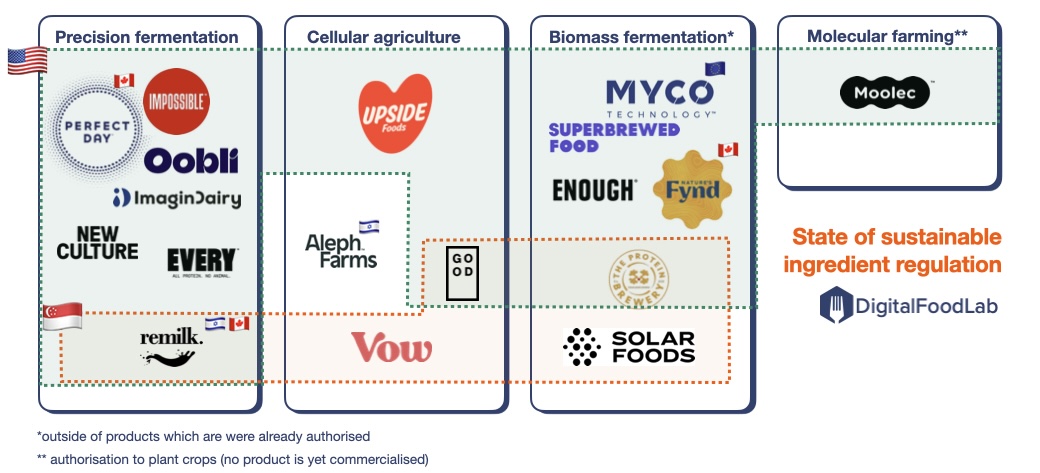

So, as I said, regulation is moving so fast that it can be hard to know where we stand. We mapped all the startups that have received regulatory approval based on their technologies (if I have missed something, let me know; I’d love to keep this mapping updated and as comprehensive as possible). If you want more on these technologies, here is our trends report with a page with definitions, examples, and applications for each.

Then, we can make three observations:

1 – It’s going fast: most of the companies have received approval for commercialisation in the past months: when making this mapping, I was always pushing the boundaries and making more room, as I was thinking about more companies that should be included. At the end of the day, I am quite surprised by the number of logos. A year ago, it would have been quite empty.

Some may still be tempted to see these different technologies as pipe dreams, they are becoming very real.

2 – Europe where are you? We hear more and more about cool European startups raising money, but they are not on this graph, because none has been fully authorised. It’s good to be slow when you want to be careful and reassure consumers, but at some point, you have to move forward. The EU regulatory body has recently rejected Perfect Day’s application, making us even more skeptical about the potential of technologies such as precision fermentation on the continent in the short or medium term.

Financing research through grants and other schemes will have its limits, and could even be judged as stupid if it only leads to have its output being valued (in terms of facilities being build, job created, tax revenue, and influence) in other places.

On the opposite, the US and Singapore are leading the rest of the world, followed by Canada and Israel.

3 – It goes beyond meat: of course, many of these companies are targeting the meat alternative market. But then again, most are looking beyond that with applications in dairy, eggs, and also sugar (such as Oobli which announced a partnership with Grupo Bimbo).

In a word: progress is impressive. Still, very few companies have yet products widely available to the public, and among them, and none is yet doing huge volumes. Following what’s happening on the regulatory front is imperative for any player involved into this space and seeking the best path of action. What you have on the mapping is about authorisations, but they are other aspects to take into consideration:

- companies seeking authorisation

- those who have failed (and which are much less keen to communicate on that)

- the evolution of the regulatory path (many countries are changing the way these technologies are regulated) which also involves some political considerations such as the recent ban of cultivated meat in Florida.

That’s something we work on a subscription basis with clients with our personalised FoodTech watch offer. If you’d be interested, contact us!